A Housing Market Slowdown

The housing market has been on a tear throughout the pandemic.

In 2021, the average sale price of a home was $346,900, a 16.9% increase from 2020.

But are we starting to see this pace slow down?

It’s not a stretch to state that the rate of price increases we’ve seen over the last few years is not sustainable.

Mortgage rates spiked the most they had in nine years in December. Furthermore, the Federal Reserve is expected to raise interest rates, with predictions ranging from three to seven rate hikes in 2022.

At the moment, the housing market in many areas is experiencing surging demand with little inventory.

It is one of the reasons why Homie, the Utah real estate market disruptor, ran into some trouble and recently announced a reduction of around 28% of its workforce.

So we have a housing market with limited supply and extremely high demand, and the Fed is set to raise rates multiple times this year — what happens next?

The Case Against Zillow (Z)

Rising interest rates and corresponding mortgage rates should start to dampen buyer demand. These conditions could also slow down other aspects of the housing market, such as housing construction and investment spending.

Limited supply and, more importantly, reduced demand could seriously cool down the housing market.

This isn’t great news if you’re a company profiting off the buying and selling of real estate, like digital-based firm Zillow (Z).

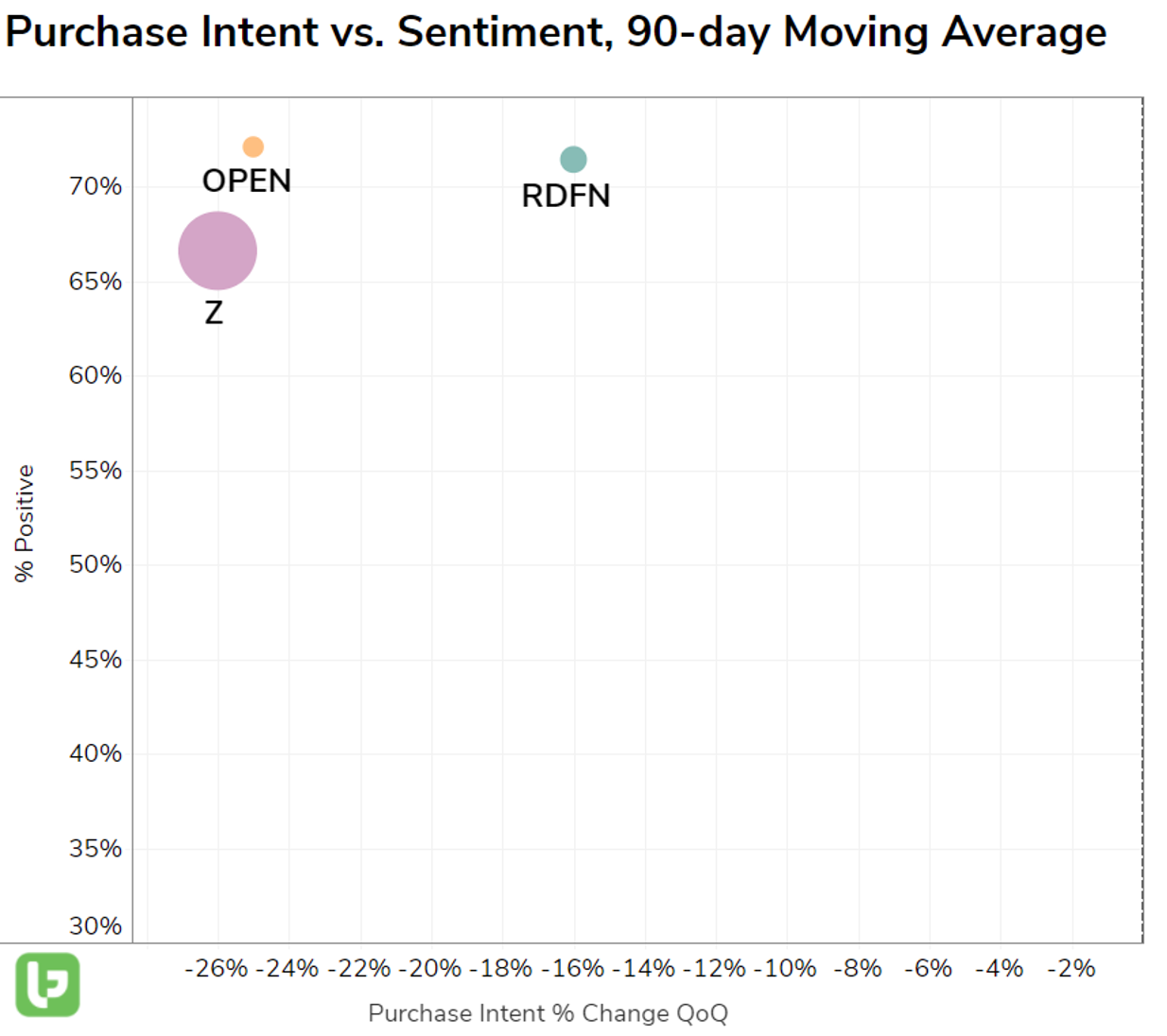

LikeFolio data reveals the company’s Purchase Intent mentions have experienced a -26% decline quarter over quarter.

You may think this is just a decline in Zillow’s business, and house buyers and sellers are using other platforms.

However, there are other factors at play.

Look at Zillow against its peers…

Compared the company to Opendoor Technologies (OPEN) and Redfin (RDFN), Zillow is in last place for both Purchase Intent growth and Consumer Happiness.

This creates an interesting scenario.

After Zillow’s most recent earnings release, the company saw its shares jump as much as 20%.

Why?

Because it is getting out of the home-flipping business more quickly and economically than it had previously expected.

But this doesn’t change the fact that Zillow’s underlying business is underperforming peers.

OK, so the stats on Zillow aren’t great.

But did you notice that Opendoor Technologies and Redfin consumer Purchase Intent mentions are also on the slide?

This is an industry-wide shift.

Redfin’s consumer Purchase Intent mentions have dropped -20% QoQ, and Opendoor’s Purchase Intent mentions have declined -23% QoQ.

According to Redfin itself, “if mortgage interest rates were to rise to 3.9%, a homebuyer with a $2,000 monthly housing budget could afford a $382,250 home.”

While that may seem minor at first glance, it is down from the $396,000 home a buyer with the same budget can afford with a 3.5% rate, which is roughly where mortgage rates stand today.

If mortgage rates rise alongside interest rates, as expected, consumer buying power will likely decrease in 2022.

What Do Real Estate Macro Trends Reveal?

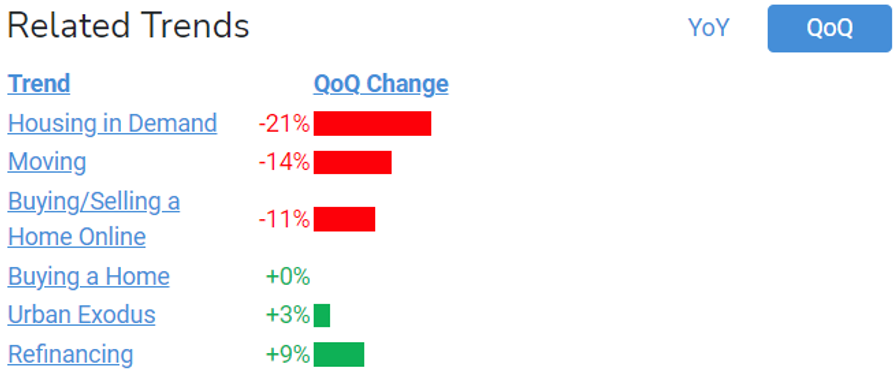

LikeFolio data suggests that many consumers who planned to move did so over the last two years.

Mentions of moving and housing demand are cooling off, with both recording double-digit drops on a quarter-over-quarter basis.

Meanwhile, many consumers are opting to refinance and take advantage of rates while they’re low, perhaps to reinvest in their existing home.

Summary: A Slowdown, Not a Crash

LikeFolio data appears to display the stars aligning in the real estate market… just not in favor of firms that profit from these transactions.

I’m not suggesting the market will experience a severe decline…

Instead, I’m highlighting that while many experts anticipate that the housing boom will continue throughout the next year, consumer insights are telling us the market is cooling off.

And when you’re facing an uphill battle, you definitely don’t want to start the race in last place.

Keep an eye on Zillow long term… An opportunity may arise to play this one to the downside.

Andy Swan

Founder, LikeFolio