A Rare Oversold Opportunity to Pounce on Today

By Lucas Downey, Contributing Editor, TradeSmith Daily

It isn’t often that you’ll find deeply oversold opportunities in quality companies near market all-time highs.

So, when it comes along, don’t stare… Prepare.

As earnings season comes to a close, arguably the biggest downside surprise is Starbucks Corp. (SBUX). The stock is off 18% since the report at the start of the month.

But should we run away from SBUX? Is the world’s most popular coffee shop chain finished?

No… In fact, I believe it’s shaping up to be a fantastic medium-to-long-term opportunity (disclosure: I’ve been a SBUX shareholder for years).

Many of you may say I’m crazy for such a bold statement given the coffee giant brewed up one of its ugliest earnings reports in recent memory:

- Sales declined 1.8% from a year earlier

- Full-year 2024 guidance was lowered

- The company also mentioned a fall-off in traffic from occasional customers

I get it… it’s not a pretty picture.

But as I like to say over and over again – if you focus solely on today, you’re undoubtedly going to miss what’s coming tomorrow.

We don’t have a crystal ball here at TradeSmith. But we have something better.

Powerful, tangible, historical analysis.

Today I’ll serve up three data-driven reasons why I see SBUX as the most deeply oversold opportunity in years.

Grab a cup of joe… let’s study this grande setup.

Starbucks (SBUX) Stock Has Lost its Way

They say the trend is your friend.

Investors seeking stocks to buy should always look for those in uptrends – stocks climbing month after month.

Though lately, Starbucks shares have been grinding lower and lower seemingly day after day. That’s the nightmare scenario that most traders try to avoid.

This one-year chart shows how the stock recently reached its weakest relative performance versus the S&P 500. Over the past 52 weeks, the S&P 500 has ripped 25% while SBUX has declined 32%:

One glance at this chart would tell most investors to avoid this company at all costs…but as I’ll show you, I believe that’s a grave mistake.

Sometimes the greatest investments come when the crowd is least interested. And when stocks reach extreme oversold conditions, they can signal glorious upside potential.

Let’s now dive into those reasons why Starbucks, in my eyes, is one of the most compelling investments for the next year…

3 Powerful Reasons to Bet on Big Upside from Starbucks

So often a stock’s price reflects the here and now. It doesn’t look at fundamental factors, which can signal a completely different picture unfolding.

The first reason you’ll want to consider dipping your toes in Starbucks stock is simple: The company has a rich history of being shareholder-friendly.Reason No 1: Starbucks Has a History of Share Buybacks

When I dive into a company’s situation, I first check on what they do with their cash. After R&D, companies typically have four ways to use cash:

- Service debt

- Issue dividends

- Buy back shares

- Or simply build up more cash by holding it in Treasurys

One of my favorite shareholder-friendly metrics that a cash-generating enterprise can employ is share buybacks.

Continuously lowering the share count not only boosts earnings per share, but it lets investors know that the company is prioritizing shareholder value.

Over the past 10 years, Starbucks has reduced its share count by 24%, with 2014’s count totaling 1.5 billion and recently falling to 1.13 billion:

While this metric is never enough to give us the green light, it’ll come in handy down the road once the share price recovers.

And I firmly believe it will, in spades. Because the next two signal studies suggest monster upside is coming.

Reason No. 2: Starbucks Has Reached One of the Cheapest Valuations in Years

No one wants to catch a falling knife… But once it harmlessly hits the ground, it’s easy to pick up.

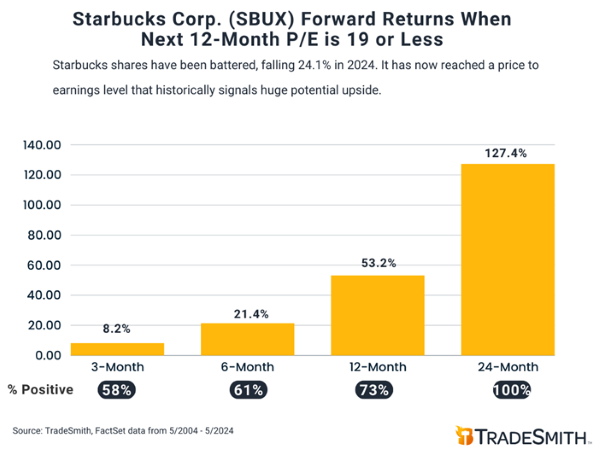

When we study Starbucks’ forward price-to-earnings ratio, you’ll see that it’s fallen to a historically low level that rarely gets this cheap.

As of Friday, SBUX sported a next 12-month (NTM) P/E of 18.66. You’d have to go back to summer of 2018 to get a similar level.

But here’s why knowing this is so critical…

Going back 20 years, whenever SBUX shares are trading at a forward P/E of 19 or lower, the forward performance is utterly fantastic.

Using weekly data, I found 98 prior instances where Starbucks traded with a forward P/E of 19 or less. Here are the results:

- 6 months later, shares gain 21.4%

- 12 months later, they caffeinate to the tune of 53.2% gains

- Be bold and 24 months later, you’re staring at an average rip of 127.4%

This is venti-sized performance:

If you’re not getting excited about this setup, I’ve got one more massive signal glaring – one that income investors will salivate over.

Reason No. 3: Starbucks Now Offers a Large Dividend Yield

You guys know I’m all about dividends. Less than a month ago I highlighted another one of my favorite opportunities I’ve owned for years, Nike.

Shares were beat to a pulp and the yield reached a level that signaled big upside. Using that same playbook, Starbucks is also screaming a buy signal.

Below you’ll find that SBUX currently sports a 3.12% forward yield. This is 50% larger than the 10-year average of 2.02%:

But here’s why this is so exciting. It’s ultra-rare for this stalwart to get a yield this high. In fact, using weekly data going back 20 years, 2018, 2020, and 2022 were the only other periods where the forward yield got above 2.75%.

Here’s why this is important. The forward return when SBUX yields 2.75% or more has been a massive bullish tailwind for the stock:

- 3 months later, the stock pops 22.4% on average

- 6 months later, it jolts 36.2% on average

- 12 months later, is a 74.3% average gain

This right here is what excites me the most for this unloved beauty:

Look… Without question, SBUX is a risky play right now.

But when you consider that management focuses on shareholder value with share buybacks… and that valuations rarely get this cheap… then you throw in that a 3%+ dividend yield is on the table – I see an outsized opportunity.

While talking heads tell you to steer clear of Starbucks because of the current picture, just know that there’s powerful historical evidence suggesting the opposite.

This is why powerful data can only enhance your trading and investing gameplan.

And TradeSmith is all about bringing you opportunities where you least expect it… driven by cold-hard data.

Stay tuned to TradeSmith Daily for more…

Regards,

Lucas Downey

Contributing Editor, TradeSmith Daily