DENIAL: Deflation Exists Now, Inflation Arrives Later

In terms of a multi-year, big-picture forecast, there is a simple acronym to remember: DENIAL, as in, “DENIAL ain’t just a river in Egypt.”

DENIAL stands for “Deflation Exists Now — Inflation Arrives Later.”

Today the U.S. economy — and the global economy, too — are subjected to powerful and persistent forces of deflation. There is a combination of moderate deflationary forces that, when all put together, create a very strong force.

The forces of deflation are so strong right now, in fact, that many investors assume they are here to stay. The world feels so deflationary, it is a head-scratching question as to how things ever change.

But the situation will change, nonetheless. Maybe not tomorrow, or even next month or next year. At some point, though, inflation is likely to come roaring back, in the style of the 1970s or even worse. The foundations are already being laid for this to happen.

First, we’ll do a quick review of the major deflationary forces in play right now. Then we’ll look at the factors that could turn them around, creating inflation’s return.

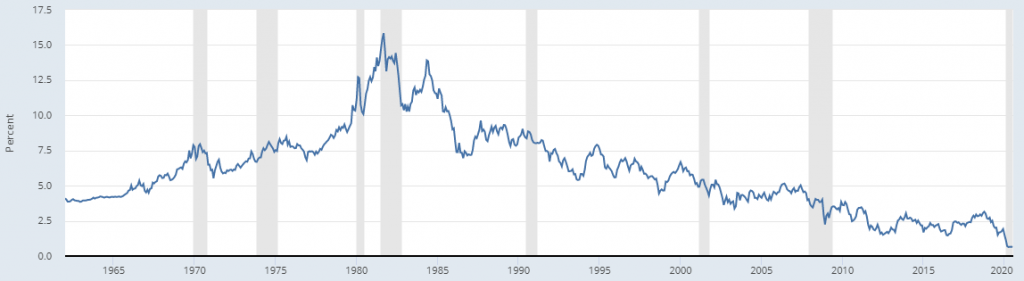

You can visually see the impact of deflation, by the way, in the long-term interest rate trend. The chart below, via the St. Louis Federal Reserve, shows the 10-year U.S. Treasury yield going back to 1962.

As you can see, the 10-year yield has been falling for decades — ever since the 1981 peak — and interest rates globally are at their lowest point in financial history, dating back thousands of years.

The stock market likes broad-based deflation, by the way, because central banks have to stimulate the economy, and try to massage credit cycles, in order to fight against it. And while central bank efforts generally don’t help the economy much, they do tend to inflate asset prices.

This is why it is common to see asset inflation in the stock market, but general malaise and deflation pressure everywhere else.

Four of the biggest deflationary drivers — forces that push prices down — are debt, demographics, technology, and trade. To briefly look at each one:

- Debt reduces growth when the debt pile gets too high. The more debt a country or company accumulates, the larger the debt service payments become. The weight of these payments turns into a drag on growth, with savings increasingly used to make payments or pay down the debt. Beyond a certain point, debt can make an economy slow down, stall, or even come to a halt.

- Demographics shrink the labor force and turn savers into spenders. As more people go into retirement, they leave the labor force, which means lower productivity, and they start spending down their retirement assets (instead of saving to build those assets). Expenditures also tend to be cut in retirement (retirees spend less). As a population ages, these factors intensify.

- Technology lowers the price of goods and services, and also puts pressure on wages. As companies figure out how to deliver more with less, the price of goods and services tends to fall over time. As companies figure out how to automate more, and rely more on software, wage levels also become more competitive. These factors in tandem drive prices down.

- Trade is deflationary through the impact of low-cost imports. Globalization means lower prices to the extent consumers can buy the lowestcost goods or find the best value for their money with an import, regardless of which country it comes from.

These forces have all been in play for quite a long time. That is why the environment is deflationary now.

But beyond a certain point, the script is flipped, and deflation pressures turn back toward inflation. Here are some examples of how that could happen:

- When a debt load becomes unmanageable, it has to be monetized. Eventually and over time, the market for U.S. Treasury bonds could dry up. If that starts to happen, the Federal Reserve will buy the bonds instead, releasing new dollars into the system (in order to buy the bonds). Those dollars will expand the currency supply and erode faith in the currency at the same time — two things that are inflationary.

- When the government takes over large portions of the economy, wages and costs rise. In the aftermath of the pandemic, “big government” is likely to get bigger than ever before. This will likely coincide with a resurgence of union jobs, an upgrade to the scope of health care benefits and worker benefits, and possibly even the backdoor installment of a means-tested Universal Basic Income (permanent stimulus checks). All these factors are inflationary.

- A rollback of globalization and “reshoring” of supply chains will raise costs. In recent years, globalization trends have gone into reverse, and realities of the pandemic will reverse them further. More countries will seek to dismantle large portions of overseas supply chains, rebuilding production facilities at home. This will raise production costs, and also create renewed ability for the local labor force to negotiate higher wages. This is inflationary.

- Supply chain choke points will raise the price of essential goods and services. The economic disruption of the pandemic created conditions for a demand shock and a supply shock simultaneously. The demand shock came from shell-shocked consumers having lower amounts of discretionary income and less ability to spend. The supply shock will come from systems and production lines that are permanently slowed down, or taken offline completely, by COVID costs.

- The U.S. dollar and U.S. treasuries will lose their “exorbitant privilege” status. While no currency stands out as a ready replacement for the U.S. dollar as the world’s reserve currency, we could be heading into a post-reserve-currency world, where dollar demand is reduced not in favor of one other dominant currency, but multiple USD alternatives. This loss of demand means demand for USD and U.S. Treasuries will fall — a development that will prove inflationary.

- There will likely be another oil-price shock — a big one — before the transition away from fossil fuels is complete. The world will eventually move away from oil and fossil fuels, switching to a mix of renewables and possibly next-generation nuclear technologies (or even nuclear fusion). But before that happens, the runway of fossil fuel demand is long enough that another oil-price shock, where demand outstrips supply in a major way, is quite possible in the next few years. As with the oil-price shock of the 1970s, this would be inflationary.

The thing to keep in mind is that nothing lasts forever. Fiat-currency regimes certainly do not. Nor do deflationary cycles largely driven by technology and globalization trends combined with leverage and credit expansion.

That which comes next — when inflation returns — will look very different than anything investors have grown used to. This is easy to grasp when recalling the 10-year interest rate chart noted earlier. Interest rates and inflation pressures last peaked in 1981, nearly four decades ago.

So, one way to think of what’s coming — especially given the chance of an oil shock mixed in — is “a return to the 1970s on steroids,” though it will also be its own beast.

This sea change from deflation to inflation, when it comes, will have a dramatic impact on markets, but not in a uniform, predictable manner. Instead, some sectors and industries will be hit hard, or potentially even crushed, by this shift, whereas others will do incredibly well.

Commodities and currencies will also roar back to life in a way they haven’t in quite a long time (though a sentiment shift in commodities, and early signals of price appreciation in precious and base metals, are already here).