Best of: How stocks could rise another 50% by 2025

Editor’s Note: We wish all U.S. readers a wonderful Thanksgiving holiday, and a warm Season’s Greetings to readers worldwide. Today and Friday we will reach into the vault and share some “best of” pieces.

The below piece ran in August of this year. It describes what could drive a slow motion “melt-up” type scenario over the next few years — and feels worth revisiting with the indexes powering to new highs.

If this scenario comes to pass, the Dow could hit 40,000, the S&P 500 could hit 4,500, and the Nasdaq Composite could hit 12,000 in the next six years. The market could even surpass those benchmarks.

Is this scenario guaranteed? Of course not. Is it realistic enough to be a genuine possibility? Absolutely.

This is one of the things that makes investing such a challenge right now. The world is in such a dynamic state of flux, there are configurations where stock prices could be cut in half and gold prices could triple or quadruple (with Bitcoin going into the stratosphere) in the next few years.

But there are also configurations where stocks rise another 50% (or even more) in the next half decade.

The “stocks rise another 50% by 2025” scenario is powered by technology, but perhaps not in the way you might think. It has to do with technology’s impact on inflation and the business cycle.

Here is the relationship that is key to understand; we’ll unpack the bullet points as we go:

- Recessions are usually caused by interest rate hikes.

- The Federal Reserve hikes interest rates to fight inflation.

- Technology is a deflationary force that absorbs inflation.

- With subdued inflation, the Fed doesn’t have to raise rates.

- With no rate hikes, multiples can keep expanding for years.

That is a lot to digest. But the basic idea is that, thanks to technology, we won’t see real inflation pressure any time soon; in the absence of inflation pressure, the Federal Reserve won’t have to embark on the standard rate hike cycle. As a result of that, the economy can keep rolling as valuation multiples expand.

Now, keep in mind, this is not a prediction of what’s going to happen. It is a plausible scenario. There are other things that can kill a bull market besides interest rate hikes. But if you remove interest rate hikes from the equation, the odds increase significantly that the expansion, and the equity bull market will last.

Keep in mind, too, there is no such thing as an “expiration date” for economic expansions. Australia, for example, has gone without a recession for 27 years and counting!

As the saying goes, bull markets don’t die of old age. Something has to kill them off, and that something is typically a series of interest rate hikes. David Rosenberg, chief economist and market strategist at Gluskin Sheff, is one of the world’s foremost experts on business cycles. This is how he recently put it:

“When you go to the causes of recession, it’s not oil, it’s not fiscal policy, it’s not trade. It’s always about the Fed. The Fed has created the conditions for every recession that we’ve seen in the post-World War II period.”

How does the Federal Reserve cause recessions? More or less by hiking interest rates. And why is the Federal Reserve willing to cause recessions through interest rate hikes? To fight inflation.

Too much inflation is considered dangerous to the economy. Under inflationary conditions, price signals get out of whack, and this eventually destroys economic growth.

When inflation is running too hot, companies lose the ability to tell whether rising prices mean “business is good” or whether inflation is creating a mirage. This leads to misallocation of resources, an outbreak of destructive behavior for consumers and businesses alike, and eventual economic implosion.

That is why central bankers are willing to cause recessions (by hiking interest rates) in the name of fighting inflation. But if there is no inflation to fight, they don’t have to take that step. This is where technology comes in.

The lack of inflation in the modern economy has been a mystery for years now. We have seen strong inflation in asset prices, but seemingly tame or missing inflation everywhere else, which left economists scratching their heads. There have been countless guesses as to why “normal” inflation is missing.

Some will argue, quite convincingly in our view, that technology is the key culprit. Technology is a deflationary force because it keeps prices down, and right now both the U.S. economy and the world are in the throes of massive technological change.

Here are some food-for-thought examples highlighting technology as a deflationary force:

- Amazon is not just a relentless force for low prices in general; it forces other companies and industries to maintain lower prices, too. Amazon is also on a constant hunt for new industries it can disrupt with superior operational efficiency, which again means lower prices.

- The “gig economy,” powered by part-time workers driving for Uber and Lyft, delivering food for GrubHub, or doing odd jobs on TaskRabbit and so on, means millions of people have switched from full-time work with benefits to sporadic contract work at a lower average wage. These “gig economy” workers don’t show up on unemployment rolls. But they have lower income with fewer benefits than before (and the better jobs they used to have are gone).

- Digital entertainment is reducing the need to buy “stuff.” If you listen to music on Spotify, watch movies on Netflix, and keep up with friends on social media, you can replace thousands of dollars worth of entertainment spending with just a few hundred dollars per year. Even expensive items like iPhones are deflationary in that, if you factor in the cost of an iPhone upgrade every three years, the cost per month is low (and falling).

- Software is making top-tier workers more productive, which makes companies more productive than before while employing fewer workers. That kills wages and increases shadow unemployment (people forced into “gig economy” jobs). When top-tier staff become far more efficient thanks to software, mid-tier and bottom-tier staff can be let go — at which point they show up in the “gig economy” instead of the unemployment line.

Those are just a handful of examples. There are many more ways in which technology is a deflationary force in the sense of keeping prices low (or keeping wage levels from rising).

Bullish analysts will further argue that, on a valuation basis, the stock market is not expensive right now. This matters because, if the argument has merit, there is room for current valuation multiples to expand.

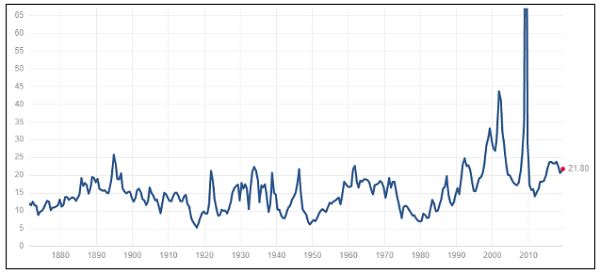

The below chart, via multpl.com, shows the S&P 500 price-to-earnings ratio dating back to the late 1800s.

The giant spike you see was a result of the 2008 financial crisis, a brief period in which corporate earnings violently collapsed, causing the “E” in the P/E ratio to implode. Putting aside that wild outlier, the current multiple of just under 22 is not extreme on a historic basis. It is a little bit high, but not wildly high.

And why is it rational for the stock market multiple to be a little bit high? In part, because corporate profits are notably high. And why might corporate profits stay notably high? Again because of technology. The same forces that keep worker wages under wraps, or reduce the need for human workers at the margins, help beef up corporate earnings.

Once again, it’s important to remember we are laying out a scenario here, rather than making a prediction. There are scenarios in which stocks decline sharply in the coming years, and most of them have wildcard variables that can’t be known in advance.

Such wild cards include the possibility of a U.S. recession or global recession, a geopolitical crisis, a government policy backlash, a new financial crisis, extreme trade war fallout, and more. And yet, if we take interest rate hikes out of the equation, the possibility of a continued multi-year multiple expansion becomes very real.

The Federal Reserve tends to wring its hands over inflation because inflation is one of the “boogeymen” central banks are paid to worry about. But technology may have killed the inflation dynamic.

That may sound wild, but then again we’ve never seen the likes of Amazon before, or the rise of a “gig economy” powered by smartphone apps, or the coming waves of mass layoffs due to software efficiency gains and large-scale labor automation.

As a result, if the U.S. economy can muddle through all of the dangerous wildcards ahead, investors may come to realize that a structurally lower inflation outlook is a feature, not a bug, of the 21st century information age.

If that realization takes hold in a big way — along with the simultaneous realization that a Fed hiking cycle could be “out of commission” for years to come — we could then see a doubling or tripling of enthusiasm levels for the “winner take all” tech stocks — the mega-winners like Google and Amazon, along with other “disrupters among the disrupted” tech plays with a strong outlook for growth in a low-growth world.

The deeper point here is that you want to be prepared for highly divergent possibilities. If you fixate on one single scenario for the next few years, whether bullish or bearish, your retirement portfolio will be in danger — because that scenario could easily be wrong or get thrown into a cocked hat.

Now more than ever, it is vital to be aware of the different configurations in which the future could unfold — and to prepare for wildly divergent scenarios, with the flexibility to go in whichever direction is required. We can do this wisely and responsibly with the help of software.

TradeSmith Research Team