Implications of the Super-K Recovery

“It was the best of times, it was the worst of times…”

You might remember that line from A Tale of Two Cities by Charles Dickens.

We reference it now, in 2021, because never before has the line been more true.

As the pandemic raged last spring, a debate raged alongside as to what kind of economic recovery the United States would have.

This debate provided an alphabet soup of capital letters, each one describing a different “shape” of recovery. Some argued for a V-shaped recovery — the most optimistic outcome. Others expected a W, which is sort of like a V with a bump in the road.

Still others called for a U shape — implying a long, flat stretch prior to a sharp bounce back — while true pessimists called for an L, meaning a drop and a long, hard slog. Nouriel Roubini, an economist with the nickname “Dr. Doom,” even proposed an “I” shape, meaning a drop straight down with no return.

In retrospect, the winner of the alphabet contest was Peter Atwater, an adjunct professor at William & Mary College.

Atwater, an expert in human behavior and decision-making, coined the term “K-shaped recovery,” implying two different outcome branches.

Those in the well-off portion of the economy had an outcome represented by the top half of the K, going up and to the right, while those less fortunate experienced the bottom of the K — down and to the right.

With kudos to Atwater (no letter joke intended), we would argue the pandemic has delivered not just a K-shaped recovery, but a “Super-K.”

The impact of the pandemic — and the various monetary, fiscal, and public health responses to it — has created the widest divergence of outcomes America has ever seen, with income inequality at its highest levels in nearly half a century.

The shape of the Super-K explains why investors, and many other observers of the U.S. economy, seem divided into two camps.

In one camp, you have those who think everything is fine — or better than fine, even. This camp has compelling data to point to (as we shall soon see).

In another camp, however, you have those who think the economic outlook is horrible. They also have a compelling suite of data points.

One such bearish analyst, James Rickards, even wrote a book titled The New Great Depression: Winners and Losers in a Post-Pandemic World. Rickards believes we are in the midst of a depression here and now. It’s hard to get gloomier than that.

And yet, even as much of the data justifies extreme gloom — Rickards filled a whole book with such data points — U.S. household net worth hit an all-time high in the third quarter of 2020, rising by 3.2% to more than $123 trillion.

And at the same time, the corporate earnings outlook is genuinely strong.

“Stocks Hit Records on Upbeat Earnings,” said a Wall Street Journal headline on Jan. 20.

“Earnings results so far have been better than expected,” the WSJ went on to observe, “with 88% of companies beating estimates through Wednesday morning.”

How can this be? How can the outlook be so good, and so bad, simultaneously? It’s because of the Super-K, and the fact that there is no such thing as “average” anymore.

We are used to thinking about economic statistics as if the U.S. economy is one monolithic entity. It is not. There are different experiences happening — the two branches of the K — and they are far apart.

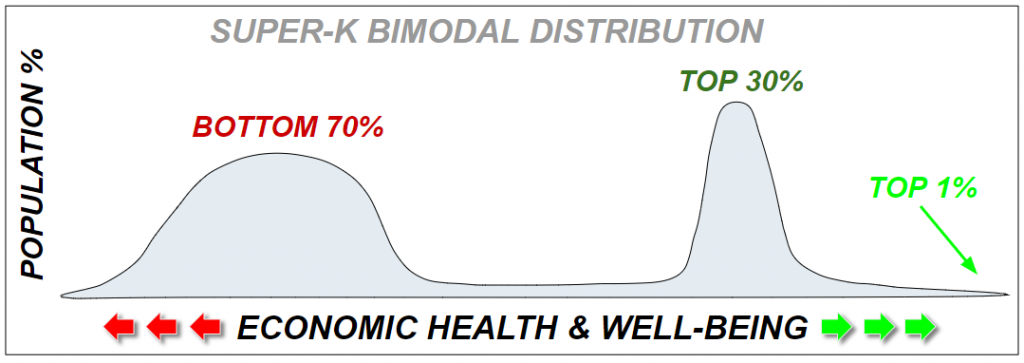

In statistics terms, U.S. economic outcomes are not following a standard bell curve distribution — the kind with a large group in the middle and outlier experiences at the tails.

Instead, the Super-K has created a “bimodal distribution,” as demonstrated in the graphic below.

In a bimodal distribution, you have two data peaks instead of one, and the peaks have different shapes.

The basic idea, as the graphic above shows, is that the top 30% of the U.S. economy is having a very different pandemic experience than the bottom 70%. Their sense of economic health and well-being is high, and for the top 1% it is off the charts.

For the bottom 70% of the U.S. economy, meanwhile, the experience has been horrible — and for tens of millions of Americans, the “New Great Depression” experience is all too real.

Why is it happening this way?

There are multiple reasons, but a big one has to do with technology.

- Knowledge workers, executives, and those doing virtual-type work like call center employees — i.e., those who can do their job with a laptop, a telephone, and a Zoom connection — did not see their workflow truly disrupted by the pandemic. They had to adopt to work from home (WFH) conditions, but by and large the WFH adjustment was a speed bump.

- Anyone whose job required a physical presence or tending to a physical flow of customers, on the other hand — a category that still composes more than two-thirds of U.S. jobs — saw their world turned upside down by the pandemic, and may have seen their business or their livelihood shut down entirely.

We can see the dramatic split in the data from the December jobs report.

The surface-level outcome for the December jobs report was ugly, with a net loss of 140,000 jobs (seasonally adjusted). But if you dig into the data, a very different picture emerges.

The December 2020 jobs report showed that the leisure and hospitality sector got crushed, with a net loss of 498,000 jobs. Those are primarily restaurant and hotel jobs, along with other forms of physical hospitality work.

Employment in state and local government positions also fell by a net 51,000 jobs, illustrating the dire state of finances at the state level. As budgets get crushed by losses of tax revenue via the pandemic, city and state employees are getting laid off.

Switch over to the technology sector, however, and it’s a whole different world.

The December jobs report showed the U.S. technology sector adding 22,000 jobs overall. Not only did the tech sector not lose employees — they posted a net gain.

And the really eye-opening number came from the IT (information technology) industry, where a whopping 391,000 jobs were added in December, according to CompTIA, an information technology trade group.

That is a stunning juxtaposition. Even as service workers and local government employees (whose jobs are largely physical, too) lost more than half a million jobs, the IT industry alone picked up nearly 400K.

Why are IT jobs in such demand right now? In part because of the pandemic.

With so many companies coordinating work-from-home arrangements and doing more with collaborative data flows and virtual meetings, more IT specialists are needed to keep everything secure and running.

The boom in tech jobs is further expected to continue into 2021. A survey from Robert Half International, a global staffing agency, showed that, out of 3,000 leading corporations worldwide, more than 90% planned to either fill IT vacancies or create new IT positions in the coming year.

And that’s not all. When you take a look up close, the disparities of the Super-K recovery are staggering.

- According to a study from Opportunity Insights, a research institute affiliated with Harvard University, American workers who earn more than $60,000 a year (the top quartile) have already seen average income levels surpass the January 2020 threshold — meaning that, financially speaking, they are already past the pandemic.

- At the same time, employment for Americans earning less than $27,000 per year (the bottom quartile) is still 20% below pre-pandemic levels. At the same time, eviction risk is soaring, hundreds of thousands of businesses have shut their doors forever, and an estimated one in five Americans live in households where there isn’t enough to eat.

One way to view the split is between two different worlds of work.

For those whose work is grounded in the physical world, the pandemic was a catastrophe. For those whose work is grounded in the virtual world, or had a natural ability to shift that way, the pandemic was a large inconvenience.

But the disparity grows wider still, because the government response to the pandemic also accelerated the divide.

The actions taken by government authorities, at all levels, widened the Super-K in both directions.

Regarding the lower half of the K, an inconsistent patchwork of lockdown rules and business closure requirements likely added to the wholesale destruction of small and medium-sized businesses, while also contributing to mass layoffs in the service sector.

But regarding the top half of the K, a multi-trillion-dollar flood of fiscal stimulus, coupled with “QE infinity,” led to an explosive run-up in the value of paper assets and a historic drop in the cost of mortgage refinancing, even as those in the top 30% of the economic strata were investing more (via fewer discretionary purchases in a pandemic) and going on a home-buying spree.

The government, more or less, made the pandemic worse for everyone who had a physical job, while simultaneously giving a huge gift to anyone with meaningful exposure to real estate or the stock market.

According to data from Fannie Mae, the mortgage giant, refinanced mortgages are being snapped up at their fastest pace in two decades, with a hunger for second homes fueling a new real estate boom.

At this point, you might be wondering two things: “When does this end?” and “How does it end?”

The answer to both questions is “nobody knows” — there are too many variables in play to pin down a reliable timeframe for when the Super-K recovery will burn itself out, or morph into something else.

But we do know that further government actions to help the bottom half of the economy — think more fiscal stimulus to the tune of trillions — will wind up doing more to juice the top half.

When the U.S. government practices a “helicopter drop” of sending money directly to people’s bank accounts, it does a world of good for Americans who are literally facing starvation or homelessness.

As a result, blanket efforts to help the tens of millions of Americans now literally experiencing Great Depression conditions can certainly be morally justified. There are better ways to do it — far more efficient, far less wasteful — but those better ways are not in place right now, and the time to act is now.

At the same time, whenever a big tsunami of fiscal stimulus washes through the economy, it is inevitably Wall Street, and the upper tier of the economy, that tends to reap the benefits first.

We saw this directly, and literally, with the $1,200 stimulus checks that millions of Americans — the ones who didn’t need the funds — wound up punting directly into the stock market.

The whole situation is wild, and unprecedented, in ways the country has never before seen. As a result of that, we can’t be sure what is next in the story.

But we do know that a perverse feature of the Super-K is that, the more the lower half of the economy suffers, the more that heroic fiscal and monetary efforts to help them wind up juicing the top half.

And that is why we can’t be sure, by any means, that the liquidity-driven mania we are living through now will end any time soon.