Is There A Maximum Trailing Stop Loss Level That Should Be Used?

This week the research team set out to investigate an interesting question. Is there a maximum trailing stop loss level that should be used across the board? We think that you’ll find the answer instructive.

By now you are likely familiar with our Volatility Quotient (VQ). It’s the first number we look at when we’re interested in a new stock. It tells us immediately how much we should expect a stock to bounce around (up or down) due to market noise.

It helps us decide what we might do with the stock. Is it a good fit? If so, how much should be bought? When should we sell? It truly is the most important number in TradeStops!

For a long time now, we’ve had our own personal rule of thumb when it comes to stocks with very high VQ’s. Personally, we never want to risk more than 50% of our capital on any stock. If a stock that we’re interested in has a VQ above 50%, then we just use a 50% trailing stop or we don’t invest in the stock at all. If we get stopped out too early in such cases, that’s okay.

We’re big believers in rules of thumb. When it comes to navigating complex systems (like the stock market), having a few simple rules to guide you is often the most effective way to get to where you want to go.

What’s even better than an untested rule of thumb, however, is when you can crunch some numbers and tweak your rule of thumb just a little bit to improve its performance. That’s what the team set out to do this past week.

To conduct this study we grabbed 7 sizable portfolios from our library of back-testing portfolios. These portfolios collectively had over 1000 buys and sells going back as far as 1998. We back-tested these portfolios using our volatility based trailing stop strategy but with a twist – we set different maximum trailing stop levels for each back-test.

Before we show you the results, we just want to make sure that there is no confusion about what we tested.

At the beginning of each trade, we calculated the VQ for the stock. If the VQ was below our Max Trailing Stop then we used the VQ as the trailing stop. If the VQ was greater than Max Trailing Stop, we used the Max Trailing Stop instead of the VQ.

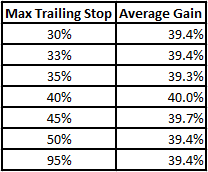

We tested seven different levels of Max Trailing Stop and we looked at the average gain across all 1000+ trades as our performance metric. The results are in the table below:

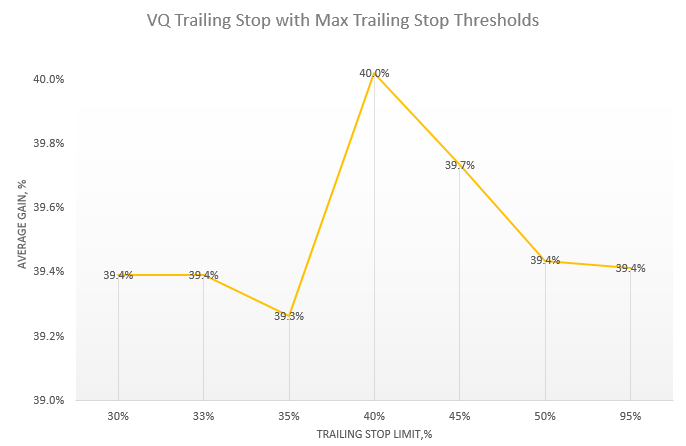

The chart below shows the same results but in a more visual way.

The horizontal axis of the chart shows the different levels of maximum trailing stops we tested: 30%, 33%, 35%, etc. The vertical axis shows the average gain of the trades for each of these different strategies.

Now admittedly, the differences in these results are very subtle. The lowest performing Max Trailing Stop was 35%. It had an average gain of 39.3%. The best performing Max Trailing Stop was 40%. It had, coincidentally, an average gain of 40%.

But it is very interesting that there is a definite peak in our test data right around the 40% Max Trailing Stop level and that the results fall off on either side of the 40% level. That’s encouraging.

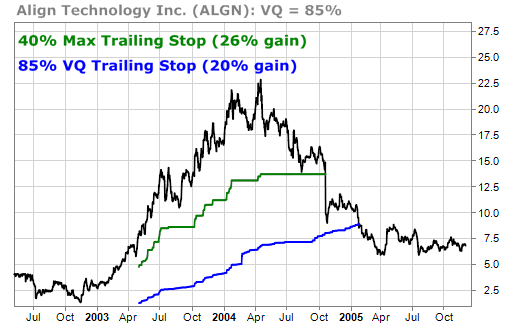

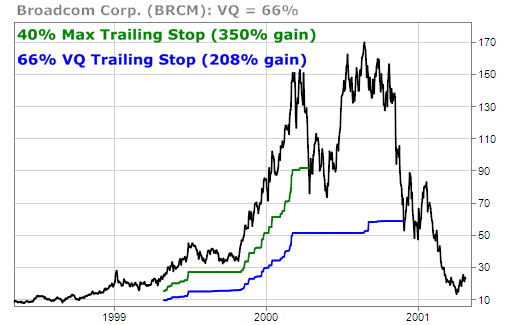

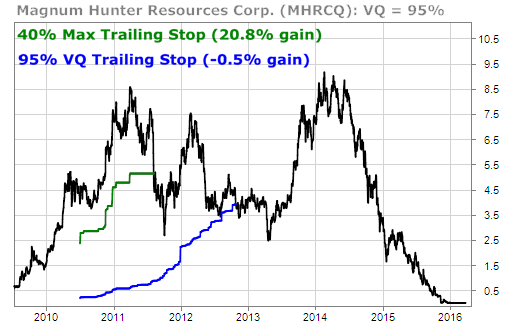

To further validate these results, we looked into the details to find a few specific trades that had a big impact on these results. Below are the charts of several that we found. In each of these cases, the VQ of the stock at the start of the trade was greater than 40% so our system just used a 40% trailing stop instead.

You can see how the 40% Max Trailing Stop strategy produced superior performance over the wider VQ Trailing Stop strategies in each of these 3 cases.

Is this a definitive study? Are we now going to change the rules of our VQ and SSI trailing stop systems in TradeStops to always max out at 40%? No. The study wasn’t large enough for me to do that and, like we said, navigating complex systems isn’t about having THE answer. By their very definition, complex systems are too complex to yield to a single answer.

Are we going to be adjusting our personal rule of thumb for maximum trailing stops based on these results? Yes. We feel more comfortable with less risk and the fact that 40% performed better than 50% across a fairly robust data set is meaningful to us.

Should you?

Your call my friend. You’re an individual investor,

TradeSmith Research Team