Asset Allocation: How a Balanced Investment Diet Builds Up Money Muscle

Editor’s Note: In this special four-part series, “Foundations of Wealth,” we spotlight the miscues to avoid, the hype to ignore, and the powerful basics to embrace. The goal: To help you win in good markets and bad — and to deliver that “edge” Wall Street hopes you’ll never find.

In my previous essay, I discussed how in the financial research business, “stock picking” gets most of the press.

People love to learn about interesting stocks with huge potential. People love to talk about stock picks, about sector trends, about new and interesting companies.

They love that feeling of being “in the know” and showing off at the neighborhood barbecue.

The mainstream financial media constantly reports on individual companies and their stock prices.

However, when it comes to lasting investment success, asset allocation is 100 times more important than stock picking.

Asset allocation is the part of your investment strategy that dictates how much of your money you place in broad asset classes.

Over the course of your career as an investor, asset allocation will have a MUCH greater impact on your wealth than stock picking will have.

The ratio will be at least 100-to-1.

Since many individual investors spend their time studying and investing in individual stocks, they don’t spend any time learning what sensible asset allocation is.

This leads them to take crazy risks with their retirement savings.

The most important aspect of asset allocation is using it to diversify your holdings across stocks, real estate, cash, bonds, commodities, gold, insurance, private businesses, and other financial vehicles.

Intelligent asset allocation is like having a “balanced investment diet.”

Ideally, you want a diversified mix of assets that greatly limits your exposure to a big decline in one asset class.

Intelligent asset allocation means you DON’T bet the farm on a single stock or even a single asset class.

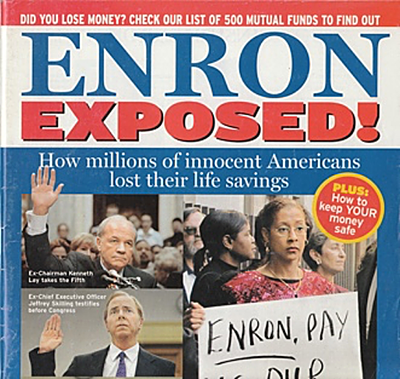

For example, there’s the story about the catastrophic losses suffered by Enron employees.

In the late 1990s, Enron was considered the world’s most innovative company. Its executives were the superstars of corporate America. So, some Enron employees placed all their retirement savings in Enron stock.

Their asset allocation was “100% Enron.”

When Enron was revealed as one of the biggest frauds in American history, its stock went to zero. The employees who bet the farm on Enron were completely wiped out.

These people used absolutely horrible and incredibly risky asset allocation.

Or consider Americans who went “all in” on real estate in 2005 and 2006.

Back then, real estate mania was in full force. Real estate was considered a “can’t lose” bet. So, many people put all their savings into real estate… and even took on loads of debt to “leverage” their returns.

When the real estate market crashed, these “all in” real estate players were wiped out.

At the heart of their downfall was absolutely crazy asset allocation.

They bet the farm on one asset class… and it was in a bubble.

If you keep a huge portion of your wealth in a single asset class — whether it’s stocks, bonds, oil, gold, real estate, or whatever — you leave yourself exposed to a large decline in the value of that asset class.

You don’t have a good financial foundation and you make yourself financially “fragile.”

You can leave yourself exposed to what happens with just one business, one stock market, or one asset class.

Given the big risks that going “all in” on one stock or one asset class presents, it makes great sense to diversify your wealth.

Think of it like eating a balanced diet.

You want to include options from different food groups. Taken together, a mix of things helps you achieve maximum health.

Some Assets “Zig” When Stocks “Zag”

According to the investment bank Credit Suisse, U.S. stocks have returned an average of about 10% per year for the past 120 years.

This average return beats gold, oil, bonds, cash, and every other widely traded financial asset on the market.

Stocks produce excellent long-term returns for a simple reason: The U.S. system of free enterprise leads to tremendous wealth creation. It gives life to value-creating businesses like Apple, Ford, Starbucks, Home Depot, Coca-Cola, Boeing, and Google.

Free people and free markets create goods and services that people want to buy — and wealth follows.

Investors go along for the ride.

Given the stock market’s long track record of success, it’s no wonder many people are interested in stocks.

However, the high returns you can earn in stocks come with a tradeoff.

Stocks are more volatile than bonds and many other assets. From time to time, stocks experience big declines in value (aka “bear markets”).

For example, when the tech-stock bubble burst between 2000 and 2002, the benchmark S&P 500 index declined by 49%.

During the bear market accompanying the Great Recession of 2007-08, stocks fell an incredible 56%.

These two recent examples show that stocks can generate excellent long-term gains, but can inflict serious short-term pain.

That risk is more than many people can afford.

And no crisis-proof “hardened” portfolio should decline in value by 56%.

Fortunately for investors, some assets “zig” when stocks “zag.”

They do well even when the stock market is struggling.

After all, the world is a big place.

The menu of assets investors can own is large and varied.

There’s rental real estate. There’s farmland. There’s timberland. There’s gold and government bonds.

There’s municipal bonds and corporate bonds. There’s cash, commodities, collectibles, and currencies.

There’s private business.

And, of course, there’s cryptocurrency, such as Bitcoin.

Different economic climates affect the price of these assets differently.

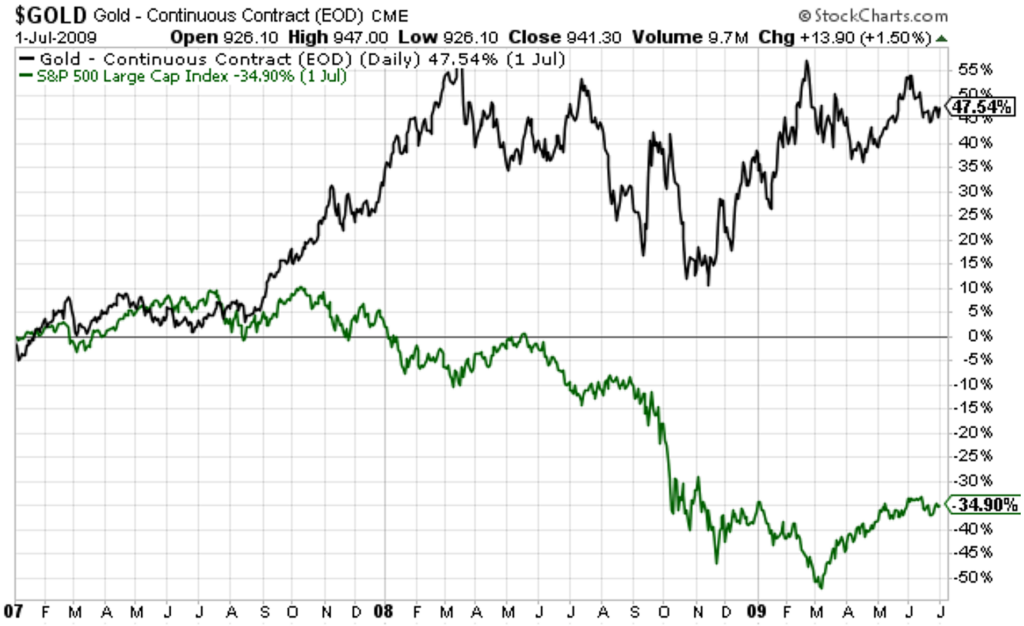

For example, in 2007, stocks began to decline in advance of the Great Recession.

As the crisis began to take hold, stocks fell throughout 2007, 2008, and 2009. The broad market fell 51.7% from its 2007 high to its 2009 low.

During that terrible period for stocks, gold — which is traditionally considered a “safe haven” asset — gained 27.8% You can see this big difference in returns in the chart below.

During the same rough period for stocks, government bonds — another traditional safe haven — climbed about 18%.

You can see this big difference in returns in the chart below:

Or consider what happened during the 2000-02 bursting of the tech bubble and the subsequent bear market in stocks.

During this brutal time for investors — where technology stocks lost over 70% of their value — corporate bonds returned 9.3% in 2000… 7.8% in 2001… and 12.1% in 2002.

Real estate also did well during the tech meltdown.

The S&P Case-Shiller U.S. National Home Price Index increased 27% from Jan. 1, 2000, through the end of 2002.

You see these kinds of divergent returns across asset classes over and over throughout history.

Because different economic climates affect different businesses and asset classes differently, some assets “zig” when stocks “zag.”

That’s why an investor focused on building wealth and maintaining it will own a diversified mix of assets.

To be clear, there’s no “one size fits all” asset allocation strategy that is right for everyone.

When you (possibly with the help of a financial adviser) think about your right “mix,” you must consider your age, your risk tolerance, and your goals.

A 45-year-old who wants to pay college tuition for three children will think about asset allocation much differently than a 28-year-old with no kids.

And a 28-year-old with no kids will think about asset allocation differently than a retired 75-year-old.

Whatever asset allocation mix you choose, just make sure you’re not at risk of being wiped out by a crash in a single business or asset class.

This will ensure your financial life is built on a strong foundation… and increase your odds of achieving total financial freedom.

Your second tool will increase it even more… I’ll describe position sizing in the next essay.