I showed you at the start of 2024 how American investors overwhelmingly buy American stocks, shunning most anything outside our borders. And for the past decade and change, that’s been a good bet. On the whole, U.S. stocks have well outperformed any other global market.

Though, that tide has spent many years going out. A reversion to the mean may be in the cards… and soon.

To play this trend, you can buy ETFs of certain country markets… or a basket of a bunch of markets… Or, the hardest thing for a U.S. investor but likely the most profitable, pick great stocks outside the U.S.

Going that route benefits from some boots on the ground in a foreign market to really find great opportunities. And there’s one guy I know of who has boots firmly planted on the ground in the South American market – Charles Sizemore from the Freeport Society.

If you haven’t already been following along with Charles in The Freeport Navigator, I highly encourage you to sign up to read for free. The letter’s principles – of pro-free markets, anti-totalitarianism, and terminally bullish on a thinking man’s ability to outwit the schemes of big government – ring loud and true in every issue.

Today, though, I want to share a bit of insight from Freeport Alpha – the premium smaller-cap investment and trading advisory whose selections don’t stop at the U.S. border.

You should know, you can only become a member of Freeport Alpha by first joining up with the large-cap focused Freeport Investor. Only then can you access their advanced strategies.

So, with Charles’ permission, I’ll also share a past recommendation from the Investor portfolio that’s still actionable today.

Let’s get tire-kicking…

Finding Hidden Gems in Latin America

Regular readers of Charles will know that he splits his time between Peru and his home state of Texas. Here’s some color from Charles on that:

You might recall that I spend most of my time in Lima, Peru. It’s the price I pay for marrying a Peruvian woman.

I’m not complaining, of course. It’s a fantastic lifestyle, and my entire family gets to experience things we’d simply never have access to back home in Dallas.

I can also tell you that Peru’s professional class appears to live on vacation. We’ll be spending the Easter weekend in Paracas, a little coastal town about three and a half hours south of Lima. Just a week ago I was in Las Delicias, a small beach town next to Trujillo, for the Feria de San Jose. Over Thanksgiving, we went piranha fishing in the Amazon.

It’s absurd. But it’s fun. And every year, the domestic travel business expands in line with the disposable income of the country’s middle class.

Barely a decade ago, travel was something that foreign guests did in Peru. It was a “gringo thing,” and you rarely saw Peruvian tourists. Those days are over, and they’re gone for good.

This has created a boom for regional companies that cater to a local clientele. But because this is still a new market, it’s also still highly fragmented and ripe for consolidation.

Observing this, Charles picked up on a little-known name in the Latin American travel space. Per Charles, we can think of it as a TripAdvisor of Latin America – a website that connects customers with airfare, hotel stays, and other travel services.

So when the company came up on his MoneyFlow screener – a powerful indicator that shows signs of rising buying volume – it didn’t take long for Charles to connect the dots.

And then he took a look at the financials. Here’s Charles again:

The company is growing like a weed. The number of smartphones that has its app installed has grown 28% year-over-year. Last quarter, revenues were up 40% year-over-year, and earnings before interest, taxes, depreciation, and amortization (EBITDA) were up 248%.

And, like most of the leading app-based platforms in the United States, the company is using artificial intelligence (A.I.) to enhance the experience and, yes, squeeze more money out of the customers.

Charles formally recommended the company after this analysis. Though, given how fresh the recommendation is, I won’t share its name here.

But it’s outside-the-box plays like these that make me really excited about Freeport Society… and excited for its subscribers. Especially when Charles has news like this to share:

Before I sign off, I have some good news to share. As I am writing this, every single open position in the portfolio is sitting on gains.

We’re going to have winners. We’re going to have losers. That’s just the nature of investing. But, for the moment, we are in a bull market. Stocks are rising and investor sentiment is positive. It will end when it ends. But until it does, it makes sense for us to continue following the money into the stocks that are powering higher.

A more logical and levelheaded reaction to an all-green portfolio you couldn’t ask for.

Again, for the time being, you can only access Freeport Alpha by first becoming a Freeport Investor subscriber.

And speaking of… let’s take a look at some of the latest research there – including an actionable recommendation.

Connecting the Dots on America’s Worsening Labor Trends

The most recent issue of Freeport Investor had to do with California’s freelance worker law, which was intended to provide certain benefits usually enjoyed by salarymen to contractors.

Sounds good… but as it often happens in government, the results are much different. Here’s Charles:

In one of the hottest job markets in history… in an economy suffering from a labor shortage… California employment fell 4.4%.

Newsom – the man who may very well be our next president if my friend Louis Navellier’s “Californication” thesis is correct – effectively killed freelancing in the Golden State. More specifically, he killed freelancing for Californians.

By chance, I happened to do some freelance work for a publisher in California last year. I had to sign an attestation that I was not a California resident and had no business nexus in the state.

In a quixotic attempt to fix a nonexistent problem that no one asked them to fix, California’s mandarin class effectively outlawed contractor employment for its own residents while allowing residents of the other 49 states – and presumably anyone overseas – to do contract work for California companies remotely.

At the center of Freeport’s worldview thesis is the idea that Californian policy often influences what happens everywhere else in the U.S. We’re seeing the same thing, with new federal guidelines put in place to redefine contract work… and potentially cause undue harm to U.S. labor trends.

But the problem is much bigger than that.

Our population isn’t growing at anything close to historical rates. Were it not for immigration, U.S. population growth would essentially be flat… and would start to shrink in about 16 years.

But the bigger story is the working-age population, or the number of Americans potentially available to work.

As you can see in the chart below, the U.S. working-age population started to flatline a few years ago and is forecast to grind sideways for the rest of this century. Barring a massive, sustained surge in immigration – which is a political nonstarter right now – there simply won’t be enough new workers coming down the pipeline to meet our labor needs.

Source: Our World in Data, United Nations

This is yet another reason why artificial intelligence (A.I.), robotics, and automation are all so critically important. We’re looking at a lost century of sluggish growth – in large part because of our elites making stupid rulings from their ivory towers, but also because of demographic trends beyond anyone’s control – without widespread adoption of these labor-saving technologies.

This makes it a powerful sector to invest in.

The big question is: What’s the best investment to make in this space?

Charles has a smart answer to that: businesses that serve small businesses – the companies with headcounts 100 and less that employ the majority of Americans.

And his pick for this trend is customer relationship management leader HubSpot Inc. (HUBS). Here’s the key part of Charles’ analysis:

HubSpot provides productivity-boosting applications for marketing, sales, and customer service, primarily for small and medium-sized businesses. True to its name, the company provides a hub that helps to funnel and track sales leads across multiple channels, including email, web searches, and social media.

[…]

HubSpot also grows with its customers. It offers a “freemium” model that allows small shops to start with a free account and then graduate to premium paid services as they expand. This makes it easy to get started, lowers the psychological barrier of getting customers to pay first, and creates loyalty with the customers.

The model works. HubSpot creates value by making a company’s sales team more efficient. And that’s only going to accelerate.

Today, the company boasts more than 194,000 business customers spread across 120 countries with an average revenue per customer of $11,520.

Back in September, HubSpot rolled out a series of A.I. tools tailor-made by the same folks that gave us ChatGPT to massively boost the productivity and effectiveness of a company’s sales team.

[…]

And the company also launched its ChatSpot.ai assistant to help users input data and run reports.

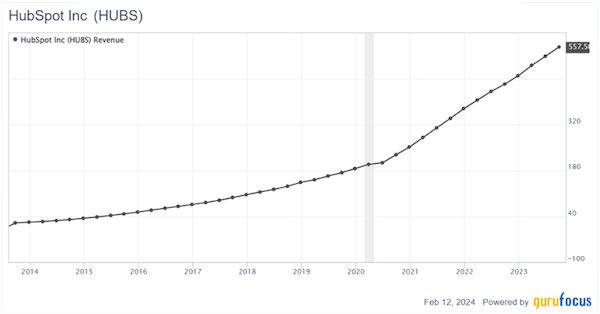

Even before adding these latest features, HubSpot wasn’t exactly hurting for new business. The company has enjoyed higher sales every single quarter for over 10 years, as you can see in the chart below.

HubSpot has grown its revenues by about 1,300% since the start of 2014 and is showing no signs of slowing down.

With explosive growth like that, there are always mild growing pains, and the company is not yet profitable on a GAAP accounting basis. But let me be clear that HubSpot is safely cash-flow positive. Its paper losses are due to high depreciation expenses from its rapid expansion and investments in growth projects (like A.I.) and from the effects of stock-based compensation (that is, paying executive stock options and employee stock-based pay).

Those expenses are real, of course. But they don’t burn cash. That’s an important distinction because it means the company’s finances are stable. I’ll take strong cash-flow profits over paper profits any day of the week.

HubSpot is exactly the kind of company I look for when I invest in “exponential progress.” It provides real solutions to up-and-coming companies that need to scale the time and talents of their workforce, even using A.I. to do it.

At the same time, the company generates exponential revenue growth for its shareholders.

I’m proud to add HubSpot to The Freeport Investor model portfolio.

As of this writing, Hubspot (HUBS) is still under Charles’ recommended buy-up-to price. And it’s up about 5% from the initial recommendation.

The company also has a foothold in the A.I. trend, offering exposure to it that’s working for real businesses now.