Tesla Will Be Added to the S&P 500 (and May Soon be a Sell, or Even a Short)

Congratulations are in order for Tesla bulls: The S&P 500 Index Committee announced this week Tesla will be added to the S&P 500 in December. Tesla shares (TSLA) jumped 13% on the news, sending Tesla’s market cap to nearly $420 billion.

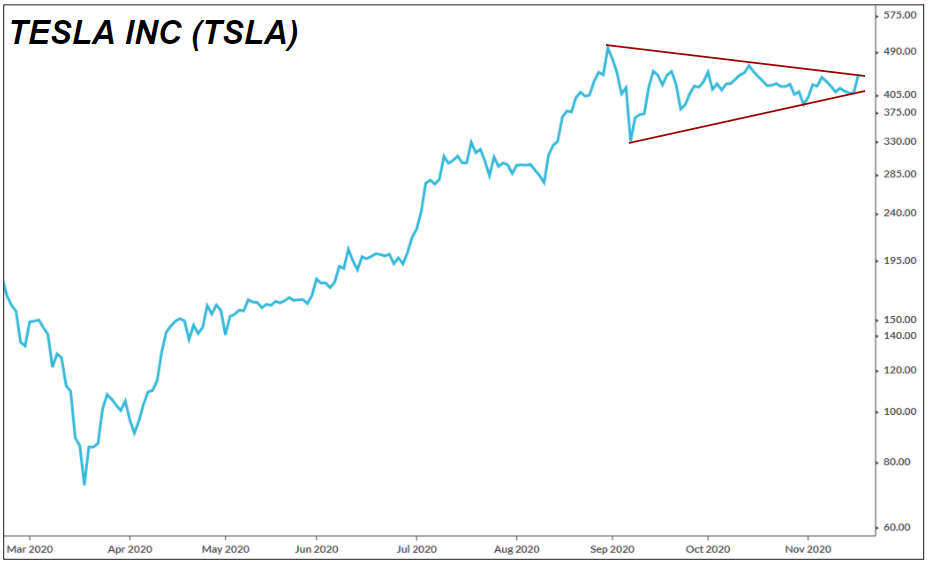

The Tesla chart is intriguing. If Tesla breaks down from here, it is definitely a sell and could even be an attractive short sale.

There is a history of wildly overhyped growth stocks reaching their valuation pinnacle, and then going into permanent decline, not long after joining the S&P 500 index. To give but one example, search your memory banks for Yahoo, a company that joined the S&P 500 almost exactly 21 years ago, in December 1999.

At the peak of its valuation, which came mere months after joining the S&P 500 — and coincided with the topping-out of the whole dot-com bubble — Yahoo was worth $140 billion.

And yet, 17 years later, in 2017, a much-diminished Yahoo was purchased for less than $4.5 billion, or roughly a 97% discount from its dot-com-bubble peak, by Verizon, a stodgy telecom.

It is very possible that Tesla, whose valuation is pure, unadulterated silliness — see the meaning of Tesla, published on Sept. 2, for more on that topic — is the modern-day Yahoo in terms of wildly inflated expectations.

It is further possible that the inclusion of Tesla in the S&P 500 is the marker of a bubble top, not unlike the inclusion of Yahoo in the same index mere months before the dot-com bubble popped in March 2000. (And make no mistake, history will note the tech bubble of 2020 to have been every bit as crazy as the one that popped in 2000.)

Note the multi-month triangle pattern in the Tesla chart below. The TSLA share price last peaked on Aug. 31, nearly three months ago. If it breaks out lower rather than higher, watch out.

In fact, if TSLA trades persistently anywhere below $400 per share from this point on, we would abandon all longs. If it breaks down and shows signs of entering a downtrend, we would consider a short sale or the purchase of puts.

The bearishness is not just tied to the S&P 500 inclusion (though that is part of it). It also has to do with the valuation, and the sheer insanity of it. Tesla today is like Yahoo in 1999 in more ways than one. It is a stock powered by fervent belief, rather than math or logic.

Entering the S&P 500 is a notable achievement and a major event. It is also a justification for buying shares before the event happens.

When a company enters the S&P 500 index, a whole universe of passive index products has to purchase shares in that company, automatically, in proportion to the expected allocation. There is an estimated $11 trillion worth of passive funds tied to S&P 500 index products. Bloomberg estimates that, when Tesla joins up, passive indexers will have to buy roughly $40 billion worth of TSLA shares.

That kind of buying commitment is certainly a bullish factor. But it is also a known factor, which means it gets priced into the shares before the event happens. This is partly why TSLA shares jumped double-digits on news that Tesla would be entering the S&P 500 in December.

Tesla will be the largest-ever company to enter the S&P 500 in terms of market capitalization at the time of inclusion. At its current market cap in the $400-billion-plus range, Tesla counts as the eleventh-largest company in the world.

Tesla’s market cap is so large, in fact, that Bloomberg estimates it will have more weight than the bottom 60 companies in the S&P 500 all put together. To make room for Tesla, the passive indexers who track the S&P 500 will not be able to just sell off the company that is getting bumped out. They will have to shave the allocation size of dozens of other holdings.

But the real problem with Tesla, as with Yahoo in 1999, is that the valuation makes no sense. There is no justification for where Tesla’s shares are priced today — not on Earth, not on Mars, not on Alpha Centauri. The math does not work. There is no plausible scenario that changes that.

Put aside for a moment the fact that Tesla’s profits are still based on the selling of regulatory credits, rather than the actual selling of cars. If not for the ongoing exploitation of a green government subsidy, Tesla would have no profits at all.

But let’s forget that for a moment, just as it appears the S&P 500 Index Committee decided to forget it. Take the $556 million in net income that Tesla reported over the past 12 months and assume they actually made it by, you know, selling cars. Then assume that Tesla ramps up its net income to $10 billion by year-end 2023.

For the sake of generosity, we are tallying up Tesla’s $556 million in regulatory credit profits as real and not subsidy driven. We are also going with the wildly fantastical assumption that Tesla will be able to ramp up its net income — not just revenue, but profit — to $10 billion two years from now.

If Tesla can make a real half-billion-dollar profit from selling cars — not credits, which will expire — and then increase that profit by 1,700% over the next few years, you still wind up with a valuation of about $218 billion as based on the average forward earnings multiple for the average S&P 500 company.

Tesla, in other words, could achieve the most spectacular, out-of-this-world profit growth scenario the bulls could hope for, and do it all within two years or less — and the stock price would still warrant being 50% lower than it is now.

But of course, there is no possible way in the known universe Tesla will achieve that kind of profit growth, because Tesla is a car company — there is software, yes, but the software goes inside cars — and as a car company Tesla has brutal competition.

Put aside the fact Tesla’s valuation is more than General Motors, Toyota, and Volkswagen put together, or the fact that all three of those players will be fiercely formidable in the electric vehicle (EV) space, or the fact that Tesla will not have a monopoly on self-driving car fleets run by municipality, or the fact that Tesla cannot claim to be the self-driving leader.

All of that matters, but for the moment we can just look at the pure-play EV competition Tesla has to contend with. Nio, a company known as the “Tesla of China,” has a market cap of $64 billion as of this writing.

If you add up the market caps of Tesla’s publicly traded EV competitors in addition to Nio — names like Nikola, Workhorse, Hylion, and Fisker — you get to $80 or $90 billion. If you then consider still-private EV companies that have raised multiple billions — like Rivian, which took a $700 million investment from Amazon — you have an EV competitor field that is worth well over $100 billion.

To grow into its valuation, then, Tesla will not only have to achieve eye-bulging, record-busting profit growth with no meaningful capex costs, at margins never before seen or even heard of for a car company, it will have to do in the presence of hundreds of billions’ worth of fierce EV competition, not just from the old guard but from a phalanx of well-capitalized pure-play competitors, many of whom the market expects to do well.

Again, there is no planet, neither Earth nor Mars, on which the math adds up. For Tesla to achieve its expected priced-in profit growth, given its current market cap above $400 billion, would be a miracle. To achieve it in the presence of competition from the old guard would be a miracle squared. Add in the competition from pure-play EV competitors and you would need a miracle cubed.

As of this writing, Tesla’s reported return on equity (ROE) numbers were in the low single-digits, around 6%, and that was with the aforementioned regulatory credits.

This is a company that will struggle to achieve even a modestly respectable profit margin, even if it executes beautifully, simply because the car industry is so brutal. And yet bulls are pricing the shares as if Elon Musk has magical powers.

From a math-and-balance-sheet perspective, it makes no sense. But from a human behavior perspective and a complex adaptive systems perspective, it makes perfect sense.

A whole bunch of people got excited about the Tesla story without doing the math or considering the competition — just as they did with Yahoo in 1999.

And the S&P 500 Index Inclusion Committee, while holding its nose at first because of the regulatory credits issue, eventually succumbed to the pressure of leaving such a high-profile company out of the S&P 500. Likely succumbing to market pressure — a very human thing to do — they said “ok” to a company whose profits are illusory and whose valuation is insane, just as they did with Yahoo in 1999.

What happens next will be interesting to watch, and possibly to trade from the short side.

We can say, too, with the utmost confidence that, unless a legitimate straight-up miracle occurs, the resolution of this story will be significantly lower share price for Tesla within 12 months’ time.

The S&P 500 inclusion news is likely the end of the game, coming near the likely end of a historic tech bubble for the ages, with more parallels to Yahoo and the 2000 dot-com-bubble endgame than one can count.