The TradeStops Sector ETF Strategy (or How to Triple the Returns of the S&P 500)

|

Listen to this post

|

Two weeks ago, we showed you how a simple strategy of using just 9 sector ETFs and following a simple set of rules could have tripled the return of the S&P 500.

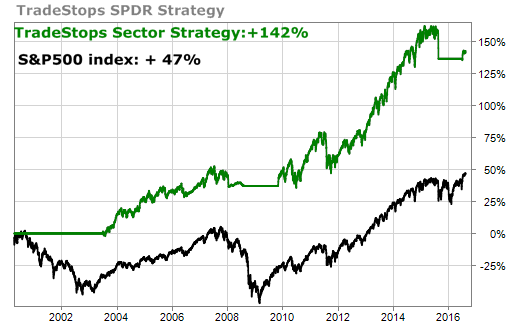

We have been inundated with emails from TradeStops members wanting more information on how they can do this on their own. Today, we will take you through a step-by-step explanation that shows you how to initiate this strategy. Here are the eye-popping results of the strategy. This study did not take into account any dividends (we will update the results using dividends in a few months).

For this strategy, we are using the following SPDR Select Sector ETFs (you can find more information about these ETFs here):

- Consumer Discretionary (XLY)

- Consumer Staples (XLP)

- Energy (XLE)

- Financials (XLF)

- Health Care (XLV)

- Industrials (XLI)

- Materials (XLB)

- Technology (XLK)

- Utilities (XLU)

These ETFs were introduced in December, 1998. The initial date of the SSI signals was March, 2000 so that is the beginning date of the study.

You’ll notice that the first trades didn’t occur until July 1, 2003. The top of the dot-com bubble in the market was in March, 2000 and the markets moved lower for the next 2-1/2 years. Also, there were no new trades from November, 2007 – November, 2009. There were exit trades only in 2008.

During market declines, the strategy requires patience as you can be in cash for an extended period of time.

Here are the rules:

- Determine the amount you want to invest in the entire portfolio.

- Determine the SSI Condition of the 9 sector ETFs.

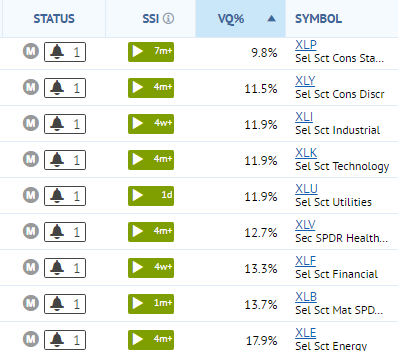

We have set up a Watch Portfolio and entered the 9 ETFs. Here is what that looks like (based on market close on 8/31/2016). We have sorted the list according to VQ%.

You can see that all 9 of the ETFs have an active SSI Entry signal in place. We also have SSI Alerts set up for all of these positions. This is critical in managing the portfolio. - Initiate this strategy only if 7 of the ETFs have an active SSI Entry signal in place.

Since all 9 ETFs are giving us an active SSI Entry signal, then we will include all 9 of the ETFs in the invested portfolio. - Determine the amount to be invested into each ETF. This is done by using the Risk Rebalancer to equalize the dollar risk in each ETF. New purchases are to be made on the first trading day of the month.

We have sorted this by the amount to be invested in each ETF. Our largest holding will be XLP (Consumer Staples) and our smallest holding will be (XLE). We have also saved this as a new portfolio. - At the beginning of the month, determine if any activity has occurred in the portfolio. If there are no ETFs that have triggered either an SSI Entry signal or an SSI stop signal, then no changes are made to the portfolio and no rebalancing is required.

- If no changes occur for 12 months, then rebalance the portfolio on the first trading day of the year. For instance, if we initiate the portfolio on the first trading day of September, and no changes occur for a year, the rebalance will occur on the first trading day of the following September.

- When an ETF triggers an SSI Stop signal, immediately sell out of the position. Keep the proceeds in cash.

- At the beginning of the month, if there are still at least 7 ETFs with active SSI Entry signals, use the Risk Rebalancer to rebalance the ETFs and the cash in the portfolio.

- At the beginning of the month, if there are less than 7 ETFs with active SSI Entry signals, do not rebalance and do not reinvest the cash in the portfolio.This is an important element of the strategy. During a market downturn, we don’t expect to see the ETFs trigger their SSI Stop signals at the same time. It could happen over the course of several months. So as the ETFs sell off, the amount of cash will increase in the portfolio.

- Stay in cash until there are 7 ETFs that give new SSI Entry signals. At that time, initiate positions in the ETFs according to rule #4.

The back tested strategy returned a total of 142% over the 15+ year study compared to only 47% for the S&P 500. And the maximum drawdown was only -17.96%!

This is not a difficult strategy to follow. From the beginning of trading in 2003, there were a total of only 168 trades initiated and most of these were for rebalancing purposes. If you set up the ETF positions using SSI Alerts, you’ll be notified of the changes that need to be made to the portfolio.

Remember, this strategy has been back tested, but no funds were actually traded. There is no guarantee that these results will be the same over the next 15 years.