This Downstream Energy Stock Has Been Inflation Proof

In the last few days, I’ve discussed the three critical parts of the oil-and-gas supply chain.

There are upstream companies that produce oil and gas. For example, companies like ConocoPhillips (COP) and Diamondback Energy (FANG) drill into the ground and extract hydrocarbons. They then sell this crude down the supply chain.

The midstream sector – which acts as a toll bridge for investors – moves fuels across the continent. These companies include pipeline operators, storage facilities, and processing firms. They tend to generate lots of income due to their favorable tax structures.

Finally, there’s the downstream sector.

This is the “end of the road” for crude oil or natural gas and related liquids. To be honest, I think that many investors forget about how important this part of the supply chain is.

When oil prices surge, the headlines focus on the producers, which own gobs of oil and gas. And investors flock to master-limited partnerships (MLPs) in the midstream due to their massive dividends.

But if you’re not paying attention to the downstream, you need to start today. This sector operates a little differently than the other two segments. That’s why you must use every tool available to determine the best downstream companies.

The Consumer’s Oil Trade

The world runs on oil.

So don’t let any doomsday prognosticators tell you that we’re facing a total end of production anytime soon. The world isn’t even close to running out of oil. British Petroleum (BP) says that new technologies can unlock so much oil in the next three decades that we see a doubling of available oil reserves.

Meanwhile, oil isn’t just a fuel required to drive our cars and power our jets. Instead, petroleum refiners use oil to make a large number of different products.

These include WD-40, asphalt, kerosene, waxes, feedstocks for cattle, and other synthetic materials. In addition, 29% of all petroleum used in 2020 was processed for 13 different products outside of motor gasoline, distillate fuels like heating oil, and jet fuel, according to the Energy Information Administration.

Now, we don’t need to talk too much about how oil refining works.

But it’s important to know a few key terms. There are three parts to the refining process. First, refiners “separate” the crude in a furnace to unlock various liquids and vapors. Since different components separate at different boiling points, it’s easy to extract those different units.

Second, these refiners engage in what is known as “conversion.” This is the process of using heat and pressure to break up hydrocarbon molecules.

The third step is “treatment.” This is the process of combining different hydrocarbons to make other products. These end-products will include the examples listed above.

The customers of these end products can include plastics manufacturers, chemical firms, and fertilizer giants.

Refiners can also sell heating fuel and natural gas products to distributors that sell these fuels to consumers.

Why Downstream is Different

Downstream energy companies have an interesting variable that separates them from their counterparts in upstream and midstream energy.

Companies in the upstream and midstream part of the supply chain tend to do better when oil prices are higher.

Upstream companies see higher share prices when oil rises because the vast reserves of crude appreciate in value. This improves the value of the assets on their balance sheet, which increases the stock.

But higher prices also increase demand from the upstream companies that are sending their product downstream.

Midstream companies do better with higher oil prices for a similar reason. Higher prices signal rising demand for end-products, which results inmidstream companies collecting more tolls as they move more crude through pipelines or into storage.

Downstream is different. These companies are likely to make more money when oil prices are declining.

The simple explanation is that lower oil prices will improve their profit margins. This is because downstream companies can buy oil and other feedstocks at lower prices. You see, downstream companies typically aren’t as likely to pass along higher costs to their customers because of existing contracts.

But this is not always the case.

There’s one company that has attracted my attention because of the current macroeconomic environment. And I want to talk about it briefly.

Rising Inflation is Okay for VLO

Now, there’s a difference between large, vertically integrated oil companies and independent downstream companies.

You see, a massive oil company like ExxonMobil (XOM) or Chevron Corp. (CVX) takes part in all three segments of the U.S. energy supply chain.

They own oil fields.

XOM and CVX pump crude out of the ground and send that oil through their pipelines.

And they refine this crude at their own plants before they send end-products like gasoline to Exxon or Chevron fueling stations.

But other companies are independent and operate in various downstream segments. They don’t produce crude or move it in midstream pipelines.

For example, Valero Corp. (VLO) is an independent company that engages in refining crude products, ethanol production, and owns gasoline stations.

Valero produces a very important product with inelastic demand: Gasoline.

Inelastic demand means that consumers are not as price resistant when the price of that product increases.

Since Americans must drive to work and use cars to get places, they will pay whatever the pump says. Other inelastic products might include medical procedures, prescription drugs, or cigarettes.

Elastic demand is different. This means that people are less likely to buy something if the price rises and more likely to buy it if the price drops.

Examples include airline tickets, sodas, or coffee brands.

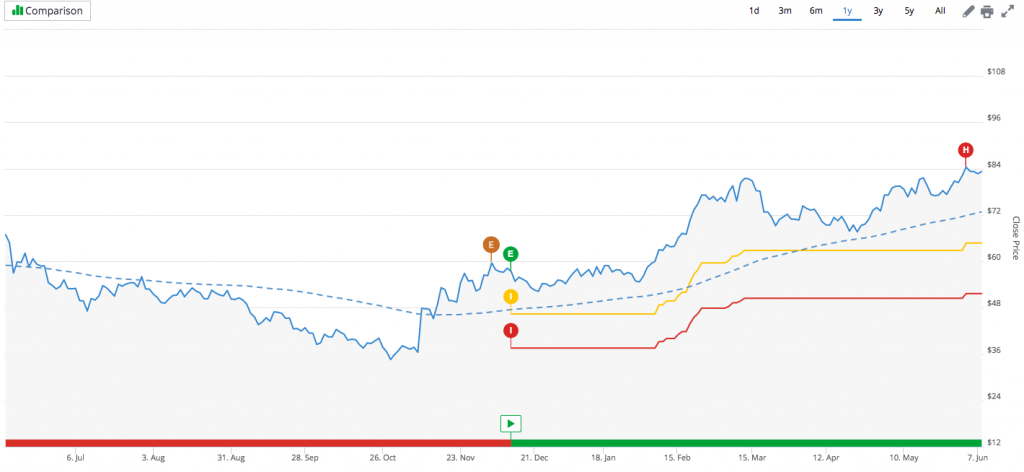

Since Valero is refining, processing, and selling an inelastic product like gasoline, it looks like a very successful business, especially with the economy reopening. The stock has been in the Green Zone and an uptrend on TradeSmith Finance for more than six months.

Of course, it has a high risk based on its VQ Score of 38.82%. But I want to put it on a watch list right now because it is a stock that qualifies for four of the TradesSmith Ideas Lab strategies: Sector Selects, Dividend Growers, Best of Billionaires, and Kinetic VQ.

Another interesting fact is that Valero has historically outperformed in periods where inflation has run higher than 2%.

According to a recent report by SeekingValue Research, the stock averaged a return of 40.4% when inflation topped 2%. Meanwhile, it averaged 46.2% when inflation topped 3%. When inflation is less than 1% for the year, the stock has averaged a negative return.

Given that the Federal Reserve is poised to let inflation run hot, I think Valero may continue its momentum despite the risks.

On Thursday, we’ll get the official reading on the Consumer Price Index (CPI). While the core reading leaves out energy and food costs, we know that inflation has been running hot.

In April, the CPI reading increased by 4.2% year-over-year. If it’s running hot again in May (the month covered in tomorrow’s report), Valero could be an excellent way to play this trend.

I’ll be back tomorrow with some other interesting ideas generated by TradeSmith.