This Legacy-Making Trade Is Hiding in Plain Sight

|

Listen to this post

|

By Michael Salvatore, Editor, TradeSmith Daily

There’s no better word than “anomaly.”

It makes no logical sense that a single sector of the market is trading so bullish, is so flush with cash, is so shareholder-friendly…

And at the same time, is the single cheapest sector in the stock market by every metric that matters.

Whatever the reason for this anomaly, it means big opportunity for you. For investors who can briefly look past the attractive veneer of big tech’s A.I. promises, it may represent the greatest deal in the stock market today.

This is the kind of thing that can turn an average-performing portfolio into a long-term super-performer. Legacies are built on trades like this.

The time to move on it is right now. Because this battle-tested market sector is dirt-cheap and gushing with cash. So much cash, it’s rewarding shareholders of this select group of companies at some of the highest free cash flow yields ever recorded. But this rare setup won’t last long. A long and strong supercycle underpinning this industry is building up, and the best opportunity to act could soon slip through your fingers.

I would not be doing my job well if I didn’t tell you about this before that happened. So today I’ll show you why this is such a big opportunity, and a simple way to play it.

Plus, read to the end to learn a bit about how you can leverage this unique opportunity in a way few investors will ever consider.

❖ I’m talking about the incredible free cash flow boom going on in the energy sector right now…

Especially in oil & gas stocks.

While big tech, A.I., and now bitcoin have captured the headlines, oil & gas stocks are quietly boasting the best return on free cash flows in the stock market.

The price/free cash flow ratio for the energy sector is at 9.6. That’s cheaper than any other, with only financials coming close at 9.7 (a lower ratio is cheaper). The next closest is real estate at a P/FCF of 19.

This ratio measures a stock’s price against how much free cash flow – aka, cash not tied up paying expenses – is coming in the door. It’s both a reflection of how ignored oil & gas stocks are, and the record free cash flows in this sector.

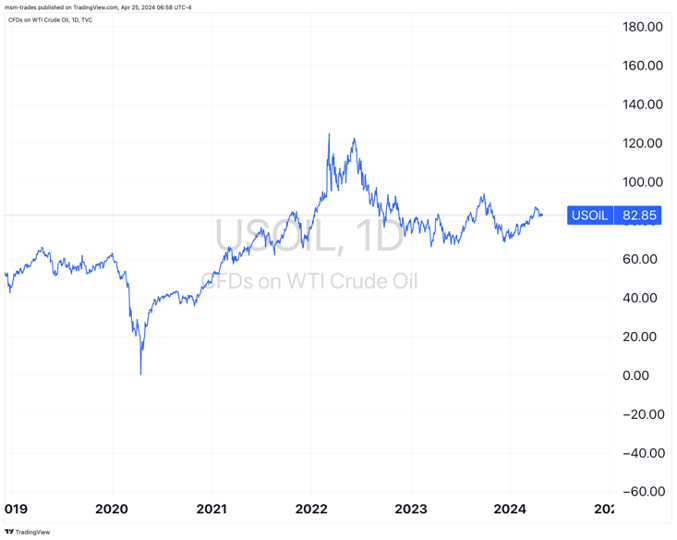

Over the past few years, oil & gas stocks have reversed their fortunes from the negative price spiral of 2020. The Russia-Ukraine war showed the world just how easily the global energy trade can buckle to geopolitical tensions. Escalating tit-for-tat strikes between Israel and Iran threaten to make the problem worse.

This has all had a big impact on oil prices. While they’ve come down from their $120+ highs in 2022, prices have settled around the $70 to $80 mark – for now (and in a minute, I’ll explain why those prices will look cheap down the road).

Higher oil prices means higher profits for oil companies… translating directly into higher profits and free cash flows… which, at the best companies, should translate into more profits for shareholders.

That’s exactly what’s been happening…

- ExxonMobil recently raised its dividend and announced a new $30 billion share buyback program, affirming its commitment to delivering shareholder value.

- Chevron has a longstanding reputation for increasing dividends annually, and it has continued this tradition with recent hikes, alongside billions in share repurchases.

- BP has not only increased its dividend but also announced plans to buy back $1.5 billion of its shares.

The share buybacks, especially, are key. Dividends reflect a company’s ability to reward shareholders now. But share buybacks reflect a company’s confidence in its ability to do so for the long term.

That’s because oil & gas companies spend a ton of resources assessing the outlook for oil demand and production going out decades.

❖ And what they see is not a world dominated by electric vehicles and solar panels…

They see a world where fossil fuels still play a major role. Even if it’s not in energy fuels, they’ll still be essential for the plastics, fabrics, and other materials used to make all sorts of goods.

As I said a few months back:

The Center on Global Energy Policy forecasts oil demand will grow by 1 to 1.5 million barrels per day each year until the end of the 2020s. In case you’re wondering, we were at nearly 100 million barrels per day in 2022. This means more and more oil will be used as time goes on.

Emerging markets are the key source of this oil demand growth. Places like India, which recently became the world’s biggest population, and countries in Southeast Asia are buying more oil as they grow and build.

Add on top the fact that oil is used for much more than just energy fuels. Oil is used in plastics, textiles, and countless other chemicals and finishings that make up products we use every single day.

That’s why I’ve said time and again that the death of oil has been greatly exaggerated. Even in a world that doesn’t sell a single internal combustion engine vehicle, oil will still have a huge role in the global economy.

And oil demand has consistently beaten expectations in 2024, thanks in part due to shipping disruptions on the Red Sea and accelerating demand from emerging markets like India. Here’s Bloomberg:

The International Energy Agency, guardian of the industrialized world’s energy security, forecasts oil demand will rise 1.3 million barrels a day in 2024.

The agency, which has had to raise its forecasts several times, now expects daily demand to average a record 103.2 million barrels this year. It points to the strength of the U.S. economy and the extra distance sailed by ships avoiding the Suez Canal as drivers of demand.

[…]

India is also set to be a major contributor of additional usage. Its government expects the economy will expand 7% in the fiscal year beginning April, making it one of the fastest-growing major economies. The world’s third-biggest oil importer behind China and the U.S., India is set to be the single largest source of global demand growth between now and 2030, according to the IEA.

“Oil demand has stayed very strong, both in the U.S. and in other countries, both developed countries and emerging markets,” said Helen Currie, chief economist at U.S. oil producer ConocoPhillips. “We’re looking for another record high in world demand this year across the board.”

This demand growth is crashing headlong into the underinvestment in new oil supply during the 2010s, after fracking brought about a domestic oil glut here in the U.S.

That underinvestment from back then is a big reason why we’re seeing such high prices today. And why we believe we’ll see much higher oil prices in the future.

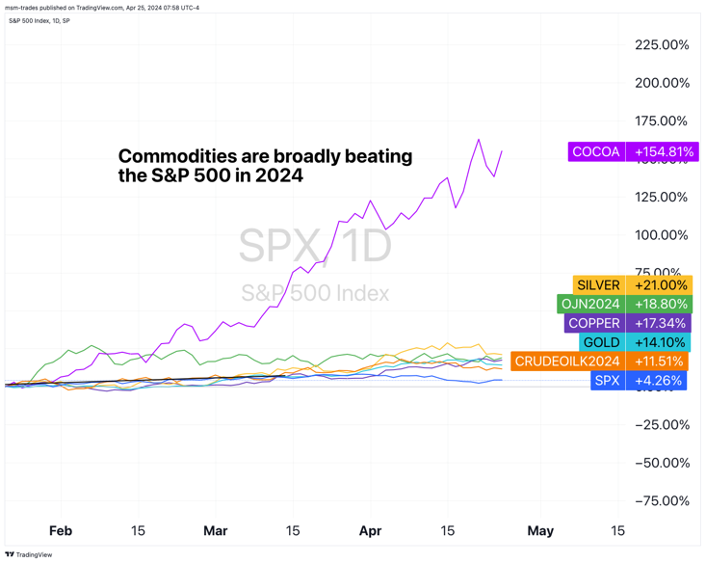

In addition, what we’re seeing in oil is just one part of a much broader supercycle across all commodities.

We’re seeing it in precious metals like gold and silver, industrial metals like copper, and even soft commodities like orange juice and especially cocoa. All of them are beating the S&P 500 this year:

Most investors are still asleep at the wheel when it comes to the opportunity in oil & gas stocks and commodities more broadly. But one eye is slowly drifting open.

You haven’t missed out. Not yet.

So how you can get involved before investors wake up?

❖ Use TradeSmith’s tools to find the best oil & gas stocks…

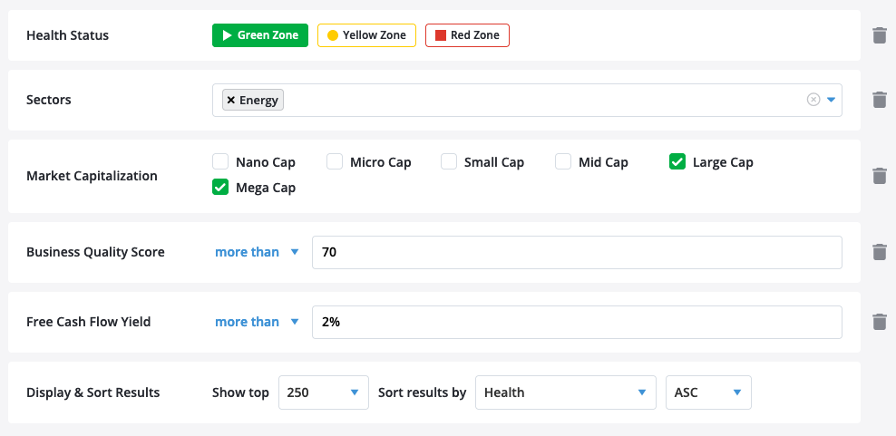

Lately I’ve been using TradeSmith’s Screener software, part of the Trade360 bundle, to find great oil & gas stock opportunities, precisely because it lets you screen for whatever you’re looking for.

I set up this screen in about 30 seconds. It returns all the uptrending large-cap energy stocks with a high Business Quality Score (BQS) – our proprietary measure of fundamental health – and with a free cash flow yield over 2%.

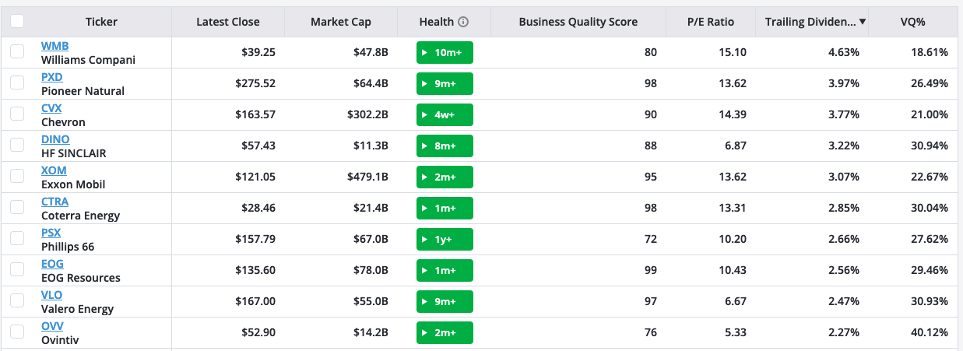

Here are the top 10 results, sorted by dividend yield:

And with these results, we can go into these individual names and see their free cash flow yields. Let’s check out Pioneer Natural (PXD)…

As of their last report, PXD sported a free cash flow yield of over 12%. As we shared recently, free cash flow yield is an excellent fundamental indicator to use when screening for high-quality, capital-efficient businesses.

PXD is also extremely shareholder friendly. You can see above that PXD pays a dividend of nearly 4%. It also recently increased its share buyback program from $17.5 billion in 2023 to $20 billion through 2025.

This is exactly the kind of thing I’m talking about with oil & gas stocks.

They’re paying out great yields, comparable to long-term Treasurys.

They’re the cheapest stocks in the market.

In fact, they’re so cheap, the leadership is happy to buy back $20 billion of stock over the next year and $2.5 billion more than they did last year. That should tell you everything you need to know.

Now, I’m confident you can do well in quality oil & gas stocks like PXD. Using our elite screening software to find them will certainly help.

But if you want to make even more money trading these names, you’ll want to consider trading covered call options on them.

When you do this, you get paid to put your stocks up for sale at higher prices. If they don’t trade at that higher price, you keep the cash. If they do, an investor buys your stock at that high price and you still get paid for selling the option.

We’ll do a deep dive on how this strategy works on oil & gas stocks next week, including a few ideas for trades that could put 50%+ annualized cash returns in your hand starting right now.

And of course, we’ll show you how TradeSmith’s tools can help you make the most of it.

Until then, get hunting for quality oil & gas stocks. There is no better arithmetic in the stock market right now.

To your health and wealth,

Michael Salvatore

Editor, TradeSmith Daily