56% of Americans Are Not “Wrong”

Last week, scores of mainstream journalists were left dumbstruck by a Guardian-Harris survey of Americans about the economy.

56% of Americans currently believe the U.S. economy is in recession.

49% of them believe the S&P 500 is down for the year.

And the same number think unemployment is at a 50-year high.

You’re reading a financial newsletter, so you probably know the opposite is true on all three counts.

But if your first instinct is to simply conclude that half of Americans are just misinformed and pessimistic, potentially for political reasons, then I’ll ask you to take a step back and really think about what these stats mean.

Despite what’s objectively a strong economy – at least in nominal terms – most Americans are struggling and feeling left behind. It feels like a recession. It feels like stocks are down. It feels like everyone is losing their job.

This feeling that things are bad… it’s not “wrong.” Things are bad for quite a lot of people. And chances are, a big chunk of that 56% number is the amount of people suffering right now.

To me, this insight quite simply overrides the hard numbers. How people feel – regardless of the facts – informs how they behave. And how people behave has huge implications for the economy going forward.

Today, I want to break from our beat of covering markets… and break out of our “investor bubble.”

We need to closely examine the American consumer – the foundational pillar that makes up 68% of the U.S. economy.

We need to understand why they’re feeling this way, and what that means about the coming elections.

And we need to learn how we should manage our own financial life to prepare.

It’s Not Just Polling – Earnings Confirm the Trend

Polling and surveys can only be so accurate. By their very nature, they can only account for a small percentage of the population – despite best efforts to make that population broad and diverse.

So where can we turn for further confirmation that folks are struggling? Company earnings reports, especially in the consumer staples and discretionary sectors, are a good start.

Recently, many of these companies have reported earnings. And a lot of what they had to show was not good.

Discount retailer Dollar General (DG) recently reported a poor profit-margin forecast due to more value-oriented consumer behavior. Even at Dollar General, people are spending less than they used to.

We’re seeing similar behavior in more discretionary names. Starbucks (SBUX) recently reported a $157 million revenue decline , its first since the pandemic, while missing earnings estimates by 12 cents per share. McDonald’s (MCD) also reported a slight earnings miss as squeezed consumers stopped eating out as much.

In the background, Walmart (WMT) reported strong earnings while growing revenues by 6% and pointed to a more value-driven middle-class consumer as the source. Meanwhile the more upper-middle-class-focused retailer Target (TGT) posted a $791 million revenue decline from the year-ago quarter and committed to slashing prices on thousands of items.

All of these company earnings reports paint a picture of a consumer squeezed into a corner. They’re buying less and watching very closely where every penny goes.

And so while it might not feel like a recession to anyone who owns stocks, or a home, or Treasurys… it certainly does feel that way for the majority of Americans who aren’t continually growing their wealth – while also struggling with price inflation.

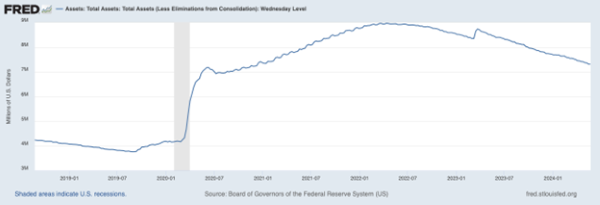

The rapid expansion of liquidity in the U.S. financial system from back in 2020 pushed prices up for almost everything… save for unspecialized labor.

I’ve shared this chart before, but it’s worth sharing again. This is the Federal Reserve’s balance sheet – the most useful proxy for the amount of money in the economy:

Currently, there are $3.5 trillion more dollars in the U.S. economy than there were at the trough in September 2019. No matter what the pace of inflation is, that’s the simple fact of the matter. Dollars are worth less than they used to be. And the only way they’ll get back to where they were is if the Fed keeps tapering the balance sheet – which it recently announced it would start to slow down.

As has been the case for many decades, wages are broadly not keeping up with everyday costs. And other data points prove how squeezed Americans truly are.

Believe it or not, a 2023 survey showed 78% of Americans “live paycheck to paycheck” – meaning they make just enough to scrape by, but not save or invest.

And this isn’t just young people or those with minimum-wage jobs. Nearly one in five Americans making between $100,000 and $200,000 claim to live this way… and the biggest cohort of this group is Baby Boomers.

That’s the reality for most people in the United States. The oldest and wealthiest generation still claims to be just scraping by. And a vast majority of Americans are in the same boat.

This is why it’s so important to break outside of the mainstream financial-media bubble – where soaring AI stocks are making investors richer.

Because it can help us forecast where this trend might take us…

The Election in Focus

The most immediate and potentially the biggest impact is on the U.S. presidential election.

I don’t personally think Biden is to blame for 100% of the inflation we’re experiencing . And frankly, no president is 100% responsible for the economy, good or bad. But they do make a great punching bag.

Most Americans see it that way… with the majority of folks who responded to the Guardian-Harris survey faulting Biden’s presidency for the economic pain.

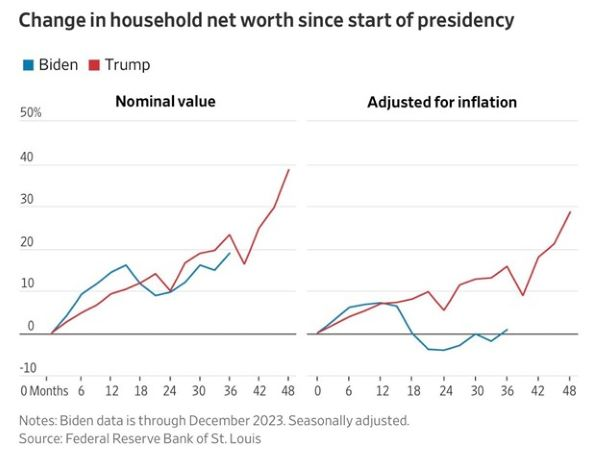

There’s also this chart from the Federal Reserve Bank of St. Louis that’s been floating around, which shows the change in household wealth by presidency, both nominally and when adjusted for inflation:

Not only is the change in household wealth for Biden actually behind Trump in nominal terms from the start of his presidency, but it’s barely above null in inflation-adjusted terms.

Again – break free from the stock market mode of thinking for a second. Only 58% of U.S. households own stocks. That means the above chart is saying just as much about wages, savings, and costs as it is about financial assets.

What this says to me, from now through the election, is that we should expect more volatility.

Consumers are rapidly changing their behavior in the face of stubborn inflation and pessimistic expectations. That will eat into corporate earnings – like I warned it could all the way back in October, in my first-ever column for TradeSmith Daily.

Continued earnings misses from major consumer discretionary companies – several of which grace the top third of the S&P 500, like Amazon, Tesla, Netflix, Disney, and Uber – would trickle through the market and cause rampant volatility.

That’s true no matter who wins in November. And that means we can’t sit idly by through the next six months and hope that the market will pull another 2023. We have to get smart about what could be coming.

Luckily, TradeSmith has thought ahead with a way to protect your wealth with a very high level of certainty… that actually benefits from high volatility.

Let Fear Pay the Bills

If you’ve been reading TradeSmith Daily the past couple of weeks, you’ve seen a lot from TradeSmith CEO Keith Kaplan and me about a specific trading strategy.

This strategy is uniquely positioned to benefit from the current environment:

- It has a 95% hit rate, with a short holding period that continually stacks up small but meaningful wins.

- It benefits when the market’s “fear gauge” – the CBOE Volatility Index (VIX) – goes up.

- It gives you the opportunity to buy world-class companies for less than their market price.

This strategy is something the ultra-wealthy investor class – the ones who don’t understand why Americans are so “wrong” about the economy – has been using for decades.

It involves making a high-odds, calculated bet on where a stock will trade in the next week.

You get paid upfront when you make the bet. If you’re right – and our world-class algorithms highlight the most likely bets to pay out – you keep all the cash.

And unlike most trading strategies, the outcome is positive if you’re wrong, too. You’d still get to buy a stock you would’ve loved to own anyway at a cheaper price – even a bit cheaper than its market value.

Keith unpacks how this strategy works in detail, including how he and our team created it, right here.

I’ll go ahead and tell you now: You do need a bit of upfront capital to get started. There’s a bit of a learning curve. And, quite frankly, it’s not for everyone.

But those who do put in a little time to master this strategy will quickly understand the opportunity the next six months hold.

Volatility is coming, whether we like it or not. The only choice we have is to harness it… or let it derail our wealth plan.

That’s why I encourage you to check out Keith’s presentation, even if you ultimately decide this strategy is not for you.

And for more on how it works, including a live demonstration, I suggest tuning in to tomorrow’s TradeSmith Daily.

Michael Salvatore

Editor, TradeSmith Daily

P.S. We here at TradeSmith have greatly appreciated your feedback over the past few weeks. Between sharing watchlists for Lucas Downey and me to size up, and your own stories of using TradeSmith’s tools to improve your financial life, it’s been a joy to read.

Today, a new prompt for you…

How have you fared in this turbulent market? Have you made any great trades so far this year? And did any TradeSmith tools help you realize that success?

Send us a message at [email protected] and we’ll consider sharing it in a future issue.