FTX Founder Sam Bankman-Fried gets 25 years… DJT revisited… The Bowie Bond… A little-understood inflation metric means an even later first rate cut… Traders are more hawkish than the Fed… But your best move is refreshingly simple…

By Michael Salvatore, Editor, TradeSmith Daily

There was a moment, not too long ago, when the suspiciously fidgety, mop-topped, sloppy-dressed Sam Bankman-Fried was the wunderkind king of the crypto world.

His trading platform, FTX, was worth tens of billions of dollars. He was worth tens of billions of dollars. And whatever he touched turned to gold.

He was also the patron saint of a trend called “effective altruism” – wherein rich people claim to want to make obscene amounts of money only so they can donate most of it to charitable causes. Thus, we should turn a blind eye to any morally bankrupt behavior in the pursuit of making that money… so long as it’s for the greater good.

But even if it was for the right reasons, Bankman-Fried got too greedy. So effectively and altruistically greedy, he took $8 billion in customer deposits at FTX and funneled them to his hedge fund, Alameda “Research.” There he and others tried to turn those billions of dollars into multiples more with incredibly risky arbitrage strategies in an already incredibly risky market.

People on the inside knew about it. They figured, “if it’s for a good cause, it’s okay.” And they quieted down that rational part of their brain that went “but what if it’s actually very not okay?”

Turns out, it wasn’t okay. Alameda failed to trade well against the crypto crash, FTX imploded, customers lost access to their funds – though mercifully, they should be made whole – and last week, Bankman-Fried was sentenced to go to prison for 25 years.

❖ Morals of the story?

Never let greed be your guide.

Never get caught up in lies.

And if you’ll excuse my French, don’t “bathe” where you eat.

On that last point, consider this: FTX was a fast-growing business and star name in the crypto world. It grew from $85 million in revenue in 2020 to over $1 billion in 2021. Growing revenue by $1 billion in a year is crazy. Crazy good.

The crypto bull market had a lot to do with it, to be clear. But it probably still would be a crazy good business, had it simply stuck to being a trading platform and had all the nonsense at Alameda never gone down.

Alas, greed got the better of it. And now, Sam Bankman-Fried has to pay for that greed with 25 years of his time on this earth. A cautionary financial tale the likes of which we haven’t seen since Bernie Madoff tried to make off with $65 billion of investor money.

This is why I insist, time and again, that if you’re going to invest in crypto, you should invest in things as far away from the terminal flaws of human beings as possible.

Keep it simple and buy some bitcoin, then store it offline. Let all the noise wash over you, and be proud not to be caught up in it.

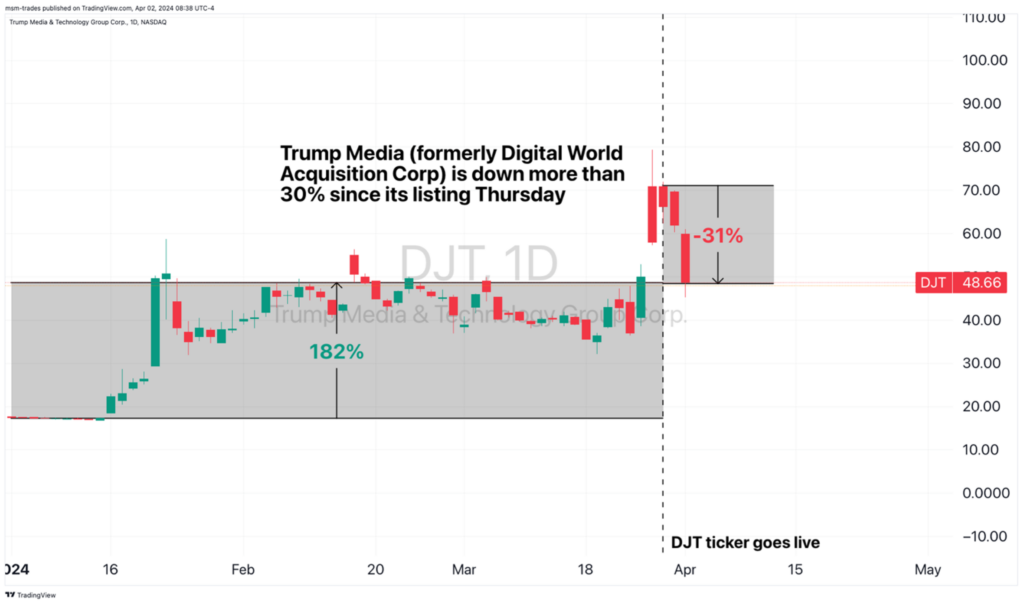

❖ Allow me to revisit the Trump Media & Technology Group (DJT) from a different angle…

If you read Friday’s TradeSmith Daily and then resolved to defiantly buy DJT as soon as the market opened on Monday morning, you’re underwater about 21%.

We proved out why it’s a bad buy from a brief glance at the balance sheet and the poor Ratings by TradeSmith metrics. Like I said then, that alone should tell you enough to stay away.

But I also recently learned that DJT, the social media company, will not report the very useful standard metrics for evaluating social media companies – like Average Revenue Per User (ARPU) and active user accounts – because it (from the 8-K filing):

…believes that focusing on these KPIs might not align with the best interests of TMTG or its shareholders, as it could lead to short-term decision-making at the expense of long-term innovation and value creation. Therefore, TMTG believes that this strategic evaluation is critical and aligns with its commitment to a robust business plan that includes introducing innovative features and new technologies.

That’s under the section titled “key operating metrics”… of which none are actually listed.

Yeah, it’s red flag city. In more ways than one.

You’re buying a social media stock that’s losing money… refuses to disclose its user base… and just listed alongside Reddit (RDDT), which while not without its problems, has a lot more to show for what it is.

But what I’ve come to understand in reflecting on DJT is that it really isn’t a social media stock. It’s equity in Donald Trump and his personal brand.

❖ This isn’t the first time we’ve seen this, but it is rare…

In 1997, David Bowie issued a novel financial instrument. It was 10-year bond that promised a 7.9% yield. The collateral? Bowie’s entire catalog of music up until 1990.

It was called “The Bowie Bond.” With a face value of $1,000 per, it raised $55 million for the genre-defying megastar. If the bond didn’t pay out its yield by maturity, the rights to David Bowie’s catalog went to investors. “Ziggy Stardust”… “Space Oddity”… “Just Dance”… all those and more. High stakes for an artist.

This is one of few times I know of where a celebrity quite literally capitalized on their personal brand… and it worked.

Despite running headlong into the difficult music streaming age of the 2000s, Bowie was able to make good on the bond and investors got their money back in 2007, with interest.

That brings me back to what DJT really represents. It’s less like owning a social media company… and more of a purely speculative momentum trade on the success of Trump and his legacy. It’s owning stock in Donald Trump.

Further, it’s a rebellion vote against both traditional media… and most other social media. Those emotions are what’s most likely to drive any upward price action.

Framing DJT this way makes it a far more intriguing, albeit far less predictable, thing to trade. It defies traditional analysis. It’s more akin to the absurd momentum in an asset like Dogecoin.

For some people, that might sound wonderful. To these ears, it sounds more like the world’s densest minefield and the sketchy promise of a pot of gold at the other end. Best to take your chances elsewhere.

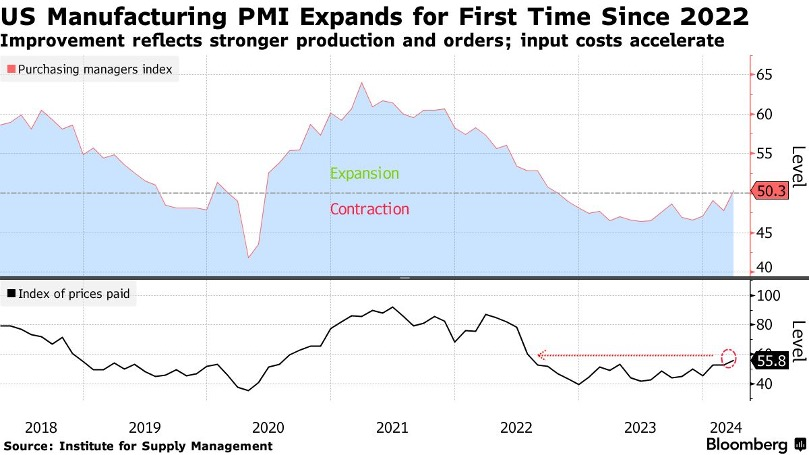

❖ ISM Manufacturing Data shows stubborn inflation… again…

At some point, we have to stop calling it an anomaly.

The Institute for Supply Management (ISM) issues a monthly gauge of manufacturing conditions in the U.S. In data released Monday, the data suggested the break of a 16-month streak in contracting (aka, recessionary) conditions.

Here’s Bloomberg:

The Institute for Supply Management’s manufacturing gauge rose 2.5 points to 50.3 last month, according to data released Monday. While barely above the level of 50 that separates expansion and contraction, it halted 16 straight months of shrinking activity.

The March index exceeded all estimates in a Bloomberg survey of economists.

Production snapped back sharply from a month earlier with a gain of 6.2 points that was the largest since mid-2020. At 54.6, output growth was the strongest since June 2022.

But here’s the buried lead:

At the same time, the cost of materials and other inputs is rising, suggesting stubborn inflationary pressures. The group’s gauge of prices paid rose by 3.3 points to 55.8, the highest since July 2022.

Higher-for-longer inflation – there it is again. And that means we’re still holding the “mixed bag” we mentioned last week.

Inflation is high. But so is growth in the U.S. economy. Rather than caving without a radical return to the “old normal,” the economy is adjusting to the “new normal” quite well.

Take the upwardly revised Gross Domestic Product numbers out late last week. The latest estimates show U.S. GDP growing at a 3.4% pace in the last quarter of 2023.

The Gross Domestic Income figure – less discussed but still important, it measures the costs incurred and income generated from producing goods and services – rose 4.8%, the biggest increase in two years.

The economy is running hot, but it’s hotter than inflation. Overall, it’s a net positive. What does that mean?

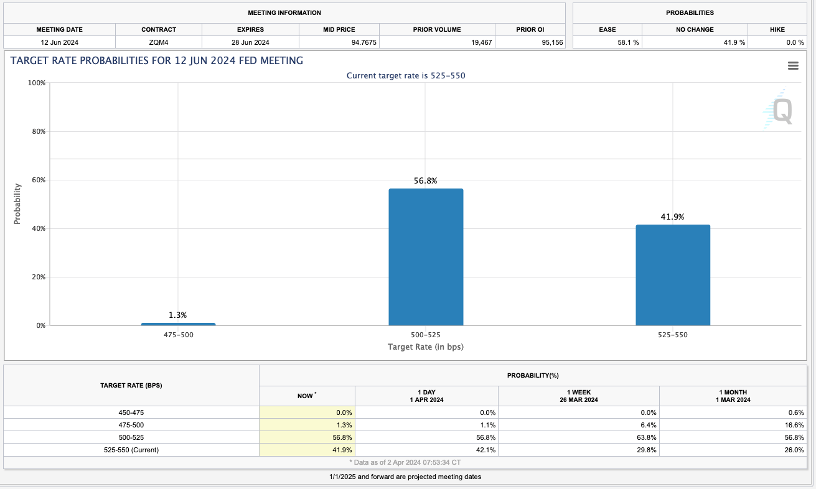

❖ Traders are finally accepting another “higher for longer”…

For a brief moment last week, bond trading activity suggested the majority of traders expect no rate cut at the June 21 FOMC meeting – what’s been seen as the most likely first rate cut in 2024. Here’s Bloomberg once more:

The amount of Fed rate cuts priced into swap contracts for this year dropped to fewer than 65 basis points — less than Fed policymakers themselves have forecast — after a report on ISM manufacturing for March exceeded all estimates in Bloomberg’s survey of economists. A bond-market decline lifted two- to 30-year Treasury yields roughly 10 or more basis points on the day, among their biggest daily increases this year.

The selloff was already under way before the ISM data release as traders reassessed the outlook for monetary policy based on economic figures and cautious comments by Fed Chair Jerome Powell on Friday, when U.S. markets were closed.

The ISM report “feeds into the narrative coming out of last week,” whereby the economy’s resilience enables the Fed “to be patient,” said Gregory Faranello, head of U.S. rates trading and strategy for AmeriVet Securities. For the bond market, that means rates stay “higher for longer.”

In a huge turn of events, bond traders are getting to be more hawkish (favoring tight monetary conditions) than the Federal Reserve.

We can see it in the CME FedWatch tool, as well, as the probability of rates staying the same at the June meeting rose from 29% a week ago to almost 42% as I write:

There’s a big “so what” here…

❖ The economy is broadly in great shape, even with tight monetary conditions and pessimistic assumptions…

And that means your next best move is refreshingly simple.

Buy the highest-quality stocks in the market… and sit on your hands.

As I mentioned yesterday, trading can be as simple or as complicated as you want it to be. But from what we see here in TradeSmith Daily, you want to err on the side of simple right now.

Everything in the data shows an incredibly resilient economy that’s bouncing back from the woes of 2022. It’s taking higher inflation and higher interest rates in stride and thriving among it all.

You have to be in stocks right now. Especially strong dividend payers and growers. There’s hardly ever a bad time to buy those, but times of above-trend growth and inflation are one of the best times.

Meanwhile, dip your toe into the small-cap sector as well. As we’ll share with you soon, historical data suggests the small-cap space is due for a Renaissance in what remains of 2024.

The train hasn’t left the station yet. But if you haven’t stuffed your suitcase with a portfolio of great names yet, get packing.