A Stock Strategy for Every Market Season – And an Income Game Plan You Can’t Afford to Miss

If you’re a longtime investor, I’m betting you know the name Peter Lynch.

Lynch was the author of the mega-bestseller “One Up on Wall Street.” And he popularized the mantra: “Invest in what you know.”

His fame – his credibility – was based on some really impressive work in the stock market… as the manager of Magellan, the flagship mutual fund of giant Fidelity Investments.

Between 1977 and 1990 – under Lynch’s stewardship – Magellan generated an average annual return of 29%.

That was enough to transform every $1,000 invested at the start into more than $27,000 by the end of that 13-year run. It’s one of the best long-term track records in the history of professional investing. And it’s practically unheard of in the mediocre world of mutual funds.

You’d probably assume that anyone smart enough to invest in Lynch’s fund made a real financial killing.

But you’d be wrong.

Fidelity itself did some research. And the company’s findings were almost as stunning as Lynch’s track record.

Not only did the typical investor NOT make 29% a year.

They didn’t make anything at all.

You heard me correctly. During a stretch that saw the fund double every two or three years, the average Magellan investor lost money.

This dismal result wasn’t just a Magellan thing.

Most individual investors earn far less than the “average returns” of the markets, funds, or individual stocks they own – for one simple reason.

Emotion.

Those investors can’t ride out the volatility they experience as they “earn” those returns.

Rather than “buy low and sell high,” as the old investing maxim tells us, most folks do just the opposite.

They ignore stocks when they’re cheap, experience “FOMO” (fear of missing out) when those shares start to run, then ride those stocks down to the point of maximum pain (and maximum losses) when those once-hot stocks roll over and fall – and end up selling at a loss.

There are variations of this scenario, but you get the general idea. Besides, all these various pathways end at the same destination – market underperformance.

And the likelihood an investor will repeat these mistakes may even be higher now than it was during Peter Lynch’s fund-managing days. Research released late last year said stocks were experiencing their most-volatile stretch in nearly 15 years.

But what if I told you there was an easy way to exit this emotional rollercoaster – forever?

What if I told you there was a simple investment approach that has returned nearly 10% a year on average for the past 100 years with surprisingly little volatility?

And that you could manage this portfolio in just a few minutes a month?

Though it sounds (almost) too good to be true, I’m here to tell you it’s possible.

If you’re a conservative investor who doesn’t want to spend any more time than necessary managing your investments, this approach may be all you ever need. But I’ll also show you how TradeSmith subscribers use it to make even better returns, too.

It all has to do with an investing mindset I refer to as “portfolio thinking” – a look at how different assets and asset classes work together to create an overall investment portfolio.

The Standard 60/40

The concept of portfolio thinking dates back to the 1950s. That’s when U.S. economist Harry Markowitz showed that investing in a combination of different asset classes — like stocks and bonds — can produce better risk-adjusted returns than you’d get by investing in either one alone.

(A “risk-adjusted return” is just what it sounds like: a measure of how much risk you’re taking to achieve a given amount of return.)

Markowitz’s research ultimately led to the “60/40 portfolio” that’s still recommended by many investment managers today. In this portfolio, you allocate 60% of your cash to stocks and the other 40% to bonds.

Again, this allocation is usually an improvement over owning either one of those assets alone. It produces far better average returns than a portfolio of 100% bonds, with less risk than a portfolio of 100% stocks.

But it does have some severe shortcomings.

First, the 60/40 portfolio is still riskier than most investors can comfortably manage.

Because stocks are historically about three times riskier than bonds, this portfolio still has the majority of its risk concentrated in stocks. If the stock market tanks, this portfolio is likely to experience a significant hit, too.

Second, this portfolio assumes that stocks and bonds are always “inversely correlated.” That’s a fancy way of saying that they generally move opposite of each other. When one does poorly, the other tends to do well, and vice versa.

And that’s not always the case.

In fact, the 60/40 strategy has come under a lot of fire lately for just that reason.

At one point last fall, a 60/40 model portfolio was down a wrenching 20% for the year. And while that mix of stocks and bonds had been a top performer – generating a market-beating 11.1% average annual return for the previous decade – researchers were quick to note that this isn’t always the case.

During the so-called “Lost Decade” to begin the 2000s, the 60/40 portfolio generated a 2.3% annual return, meaning investors would actually have lost money on an inflation-adjusted basis.

In short, despite its “balanced” reputation, the 60/40 portfolio tends to outperform when stocks do well, and it tends to underperform when stocks struggle.

At best, we can say that stocks and bonds can experience a dynamic correlation over time.

A Billionaire’s Secret

Here is where a man named Ray Dalio comes in.

Dalio is probably the best investor most folks don’t know. He’s the founder of Bridgewater Associates, the largest hedge fund on the planet with more than $150 billion in assets under management (AUM). And he’s No. 83 on the Forbes World Billionaire Index.

Dalio is also one of the first investors to truly closely study the problems with traditional portfolio strategies. And he made some fantastic insights that have greatly influenced our work here at TradeSmith.

One of his key contributions: a concept known as “risk parity.” He demonstrated that the most successful investors don’t allocate their portfolios based on the amount of money invested in each asset or position. Instead, they allocate their portfolios based on the amount of money at risk in each asset or position.

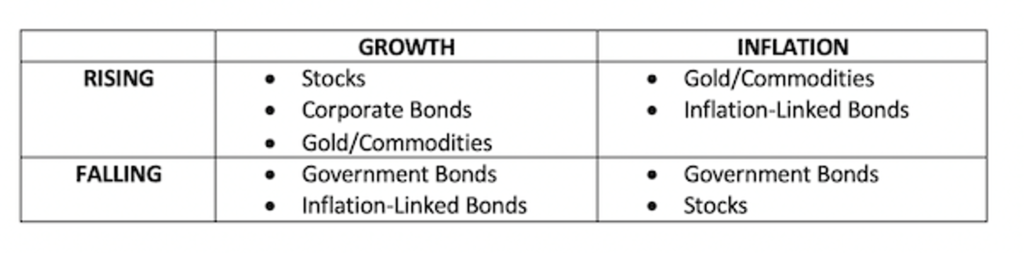

Dalio also identified four primary market environments – or “seasons” – that move asset prices. These are:

- Higher-than-expected inflation.

- Lower-than-expected inflation (or deflation).

- Higher-than-expected economic growth.

- Lower-than-expected economic growth.

He then mapped out the major asset classes by the season in which they perform best, like so:

Dalio combined these ideas of “risk parity” and “market seasons” to create what he called the “All Weather” strategy. He designed it to manage his family’s investments. But he eventually opened it up to his wealthy hedge fund clients as well.

This strategy consists of a diversified, global portfolio of up to 40 different investments, with risk spread equally among the four quadrants we detailed above.

In other words, while it may own different numbers and types of assets in each of the four seasons, it risks an equal amount of money (25%) in each of them.

Don’t Forget Income

The idea behind the strategy is both simple and brilliant.

If there are only four primary seasons that drive asset performance — but it’s difficult (even impossible) to predict when any specific season is likely to arrive — a well-balanced portfolio should be able to perform well in any of them.

Dalio designed the All Weather strategy to do just that. And it has certainly delivered so far. Since its inception in 1996, this strategy has generated close to 10% average annualized returns.

That’s virtually identical to the returns of a conventional 60/40 portfolio over the same period. But it has done so with roughly half the volatility and with significantly smaller drawdowns than the traditional portfolio.

And testing that reaches further back underscores its consistency.

From 1978 until March 2022, a hypothetical $10,000 investment in the Ray Dalio All Weather Portfolio would have grown to $520,000.

With a compound annual growth rate (CAGR) of 9.34%, the portfolio outperformed its risk (7.94%) by 140 basis points.

Unfortunately, folks like you and I can’t invest directly in Dalio’s portfolio. Bridgewater is no longer accepting new investors in the All Weather strategy, but you needed at least $100 million in investable assets to qualify even when it did. And the specific asset allocation used in the strategy has never been made public.

However, several years ago, in an interview for Tony Robbins’s book “Money: Master the Game,” Dalio did reveal a simple, “do it yourself” version of the All Weather strategy that any investor could follow.

The performance of this “All Seasons” portfolio, as it has since become known, has been impressive as well.

It, too, has generated an average annual return of nearly 10% – this time going all the way back to 1927. Yet it has done so with significantly less volatility – and smaller drawdowns – than either the market or a conventional 60/40 portfolio.

For example, over those 93 years, the All Seasons portfolio suffered just 17 losing years (18%) – versus 25 losing years (27%) in the S&P 500. And the average loss in those years was less than 4%, compared to more than 13% in the S&P 500.

I’d love to hear what you think about these ideas at [email protected]. As always, I can’t personally respond to every letter, but I read them all.