Social Security Is Failing Fast – Here’s What to Do

Michael’s note: Two years ago, our CEO Keith Kaplan penned an essay showing how Social Security was set to run out of money in 2035 and what soon-to-retire investors could do about it.

The next year, the projection moved to 2033 – and so we updated the essay with new ideas.

This year, Social Security’s failure date moved ahead another year… to 2032.

Social Security isn’t just destined to fail. Each year, the rate of failure accelerates.

And as Keith will show you below, that makes one type of data-driven investing more important than ever.

So if you’re planning to retire in the next five years (or sooner), this is a must-read… Check it out below.

Social Security is failing even faster than anticipated.

And that’s not some exaggeration meant to scare you. The U.S. government says so itself.

Last year, the Social Security Board of Trustees projected that the fund covering retirement benefits would run through its reserves in early 2033. This year, it moved that date even closer… to 2032.

Assuming no change in the trend, the government projects Social Security retirement checks will drop to 78% of what they are now – a 22% cut the moment the fund runs dry.

If that happened today, the average monthly check of $2,071 for retirees would drop to about $1,615.

So, Social Security is failing faster than the government was forecasting just a year ago.

That’s the impact facing the roughly 70 million Americans who count on Social Security today – and the tens of millions more set to retire in the decade ahead.

What can the government do to fix this?

Three things, none of which are great… and none of which any politician seems willing to do:

- Raise income taxes. That’s out the door with the recent extension of the 2017 tax cuts.

- Raise the age when you can start to receive Social Security – probably the most viable path forward.

- Cut Social Security benefits beyond what they’re already expecting to do.

If you’re coming up on retirement, you must consider a “Plan B” if you don’t want to spend your golden years working. And if you’re decades away from retirement, the Plan B is more like a Plan A.

The government is not coming to save you from Social Security’s collapse.

Luckily, we at TradeSmith have thought through this problem.

We’ve devoted our team of dozens of data scientists, software engineers, and analysts to the task of helping you make returns that outpace the market. We’ve spent tens of millions of dollars in the pursuit of this mission.

Beating the market, especially in a time of high inflation, is the best possible way to build the kind of nest egg that will endure for decades.

And even if you’re just getting started today, we have a plan for you to supplement the extra income you’re going to need in retirement when, not if, Social Security goes bust…

Your Three-Step Backup Plan for Social Security’s Collapse

Creating a backup plan for your retirement is simple in theory but may be difficult in practice.

Luckily, the hardest step is the first one. So, let’s start there.

1. Eliminate all high-interest-rate debt and ideally be debt-free.

Don’t sit on any short-term, high-interest-rate debt (basically, everything but your mortgage and maybe your car loan). It demolishes your monthly income… and hands your hard-earned money over to the banks for no good reason.

If you have debt, especially credit-card debt, make paying it off your top priority before you move on to steps 2 and 3.

I’m serious. You can’t proceed until this is done. No passive income stream or capital gains will be enough to consistently offset a credit card balance growing at a 24% average annual rate.

Downsize… stop relying on credit cards… and make a smart spending plan where you pay off the debt, period.

2. Build up your rainy-day fund.

This looks a bit different for retirees than it does for working people, but it’s just as important.

You need a chunk of cash saved away for emergencies — necessary home or car repairs, unexpected medical expenses, stuff like that.

This is the middle ground between the three steps for a reason. You can’t have too much debt… but you also can’t be so invested that you don’t have any cash on hand.

How much emergency cash you’ll need will vary on your situation. If you’re working, three to six months of living expenses is a good bet.

But if you’re already retired and looking for an estimate, just think about the most likely kind of major unexpected expense you’d face…figure out what that would cost…and then double it. This is the minimum amount of cash you need on hand. Ideally, you keep that in safe, yield-bearing assets like U.S. Treasury bills you can tap into at any time.

3. Invest in a mix of U.S. Treasurys and high-quality, dividend-paying stocks.

Now that your debt and savings are squared away, we get into the part where TradeSmith really can help: investments.

To build the core of your backup plan, you need to invest in assets that generate income while you sleep. This is critical to anyone’s wealth plan, and it should be done as early in your financial journey as possible.

Think about Berkshire Hathaway. Right now, Warren Buffett’s legendary firm is using its $397 billion war chest to earn about $14.4 billion a year in short-term Treasury bills, rolling them over and taking the proceeds month after month.

One of the most successful investment firms of all time is using the same tools you and anyone else can use to stay ahead.

Treasurys should be roughly 10% to 20% of your income portfolio as a retiree, depending on your personal risk tolerance. Go for the shortest terms and the highest rates to minimize risk and maximize returns.

If you’re not a retiree, T-bills should be where your cash savings live.

And as for the remainder, that’s where we start to talk about dividend-paying stocks.

Dividends Are Your Retirement Lifeline

Dividends are a slice of a company’s earnings, paid directly to shareholders. They’re an essential component of any retirement portfolio.

After all, while Treasurys might help you stay ahead of inflation… stocks can do much better because they appreciate in value while you get paid.

Now, not all dividends are created equal. Many dividends, especially those with attractively high yields, are not sustainable. Even small dividends may not be, either, if the company hasn’t been paying them for long or has a volatile business model.

That’s why it’s so important to focus on quality companies when you go to build a long-term dividend portfolio.

Normally, this would require a lot of time doing research.

But here at TradeSmith, we’ve built two incredible tools that help you manage all of this in seconds.

The first is our Quantum Score. This ratings system highlights stocks with all the hallmarks of a great trade – strong earnings, revenue, and profit-margin growth alongside price strength and institutional-scale buying volume. The higher the score from 0-100, the better the buy.

The second is our Screener. With it, you can quickly screen for stocks that meet any criteria you’re looking for.

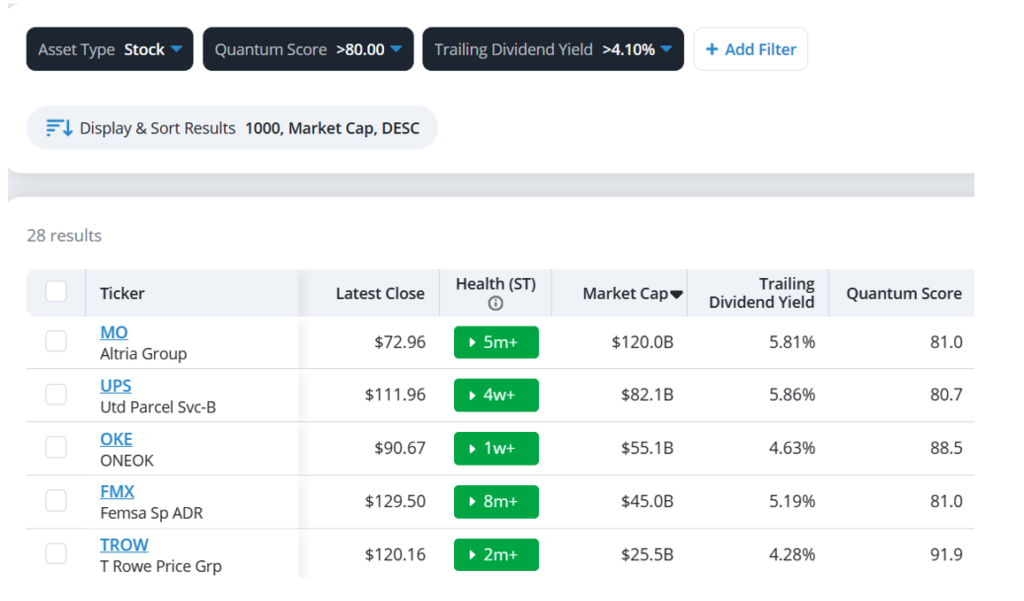

In our case, we can use it to find stocks with a high Quantum Score (above 80) plus dividend yields that beat inflation (That’s currently running at 4.2%, using the latest Consumer Price Index reading.)

That takes thousands of U.S. stocks and whittles them down to just 28. Here are the top five ranked by market cap (To our Platinum subscribers who receive everything we publish, you can easily find the rest of the stocks on this list by entering the same filters into our Screener):

All of the above stocks score above 80 on the Quantum Score, indicating a healthy combination of fundamental and technical factors. They cover tobacco, parcel delivery, natural gas utilities, consumer goods, and asset management.

All of them yield more than 4.2% – some even 5% and close to 6%. At today’s prices, their dividends represent an annual income stream that well outpaces current inflation rates.

And they’re all in our Short-Term Health Green Zone – our most sensitive trend indicator that tells you if a stock is in a healthy uptrend (Green), a caution zone (Yellow), or a breakdown (Red). Some of these signals, like in ONEOK (OKE), fired in just the last couple weeks.

With just these few parameters, we have a list of high-quality, uptrending, diversified dividend payers.

That’s a great start for someone building a high-income and high-performance portfolio… or for someone who’s simply looking for new ideas for stocks to buy.

Whatever form Social Security takes in the coming years, chances are good you don’t want to depend on it to keep you afloat through your golden years.

You have to take action, and we’ll keep showing you our favorite ways to do this here in TradeSmith Daily.

All the best,

Keith Kaplan

CEO, TradeSmith